I view Walmart’s results and comments as particularly noteworthy given their retail prominence and focus on low prices. I have previously commented on their quarterly management call comments; these previous posts are found under the “

paycheck to paycheck” tag.

Here are various excerpts that I find most notable:

comments from Doug McMillon, President and CEO, page 5:

Walmart U.S. again delivered positive comp sales, and I’m encouraged by the customer traffic trends. I’m particularly pleased by the customer response to our Neighborhood Markets, driving strong comps again this quarter. Based on recent surveys, we know that many of our U.S. customers are using their tax refunds and the extra money from lower gas prices to pay down debt or put it into savings. They’re also using these funds for everyday expenses like utilities and groceries. That’s where we can be their destination of choice. We’re not where we want to be in every store, but I’m pleased with the progress that I’m seeing.

comments from Claire Babineaux-Fontenot, EVP and treasurer, page 8:

The last item I’ll leave you with today is share repurchases. The company repurchased approximately 3.5 million shares for $280 million during the quarter. Market conditions, general business trends and a focus on maintaining our AA credit rating, among other factors, influenced our share repurchase activity. We have approximately $10 billion remaining on our existing share repurchase authorization.

comments from Greg Foran, president and CEO of Walmart U.S., page 9:

This quarter we began executing this plan. We took the initial steps in April towards a stronger investment in our associates by raising the minimum starting wage for all hourly associates to $9.00 per hour. As a part of our $1 billion investment in our associates we also raised the floor and ceiling on pay bands in our stores creating raises for many full and part-time hourly associates at every level. More than 500,000 associates benefited from this change. We’re also restructuring the management teams in the stores adding back almost 8,000 department managers. These department managers will have responsibility for a smaller area of the store ensuring that they have the knowledge and the time to engage with both the customers and store associates driving an overall better experience. The $1 billion investment in our associates this year includes training programs as well.

comments from Greg Foran, president and CEO of Walmart U.S., page 10:

With these steps in mind, let’s move on to our first quarter results. Net sales grew $2.4 billion, or 3.5 percent, versus last year. For the 13-week period ended May 1, comparable stores were up 1.1 percent, which was within our guidance. Comp sales were driven by solid growth in traffic, which was up 1 percent. Customers continue to see the benefit of lower gas prices versus last year and are responding favorably to some of our new assortments for the spring and summer selling seasons.

All formats had positive comps for the quarter, including our traditionalformat Neighborhood Markets, which posted approximately a 7.9 percent comp. A focus on customer service and in-stock position drove strong traffic in this format. Customers continue to see the benefit of Neighborhood Markets to meet their everyday needs, including convenient access to services such as drive-thru pharmacies and fuel stations.

comments from Greg Foran, president and CEO of Walmart U.S., page 11:

Moving on to the remainder of our financial results…In the first quarter, gross profit rate declined 13 basis points driven primarily by a headwind from shrink, half of which was in food. We are addressing this increase immediately, bringing a high level of focus and visibility to this concern by adding it as a key urgent agenda item this year. In addition to shrink, the ongoing mix shift in pharmacy, incremental expenses related to the west coast port congestion, and cost inflation in consumables contributed to the decline. Somewhat offsetting this was a continued focus on the urgent agenda items laid out last year, including managing throwaways in fresh and reducing inventory that is no longer active in the stores.

_____

The Special Note summarizes my overall thoughts about our economic situation

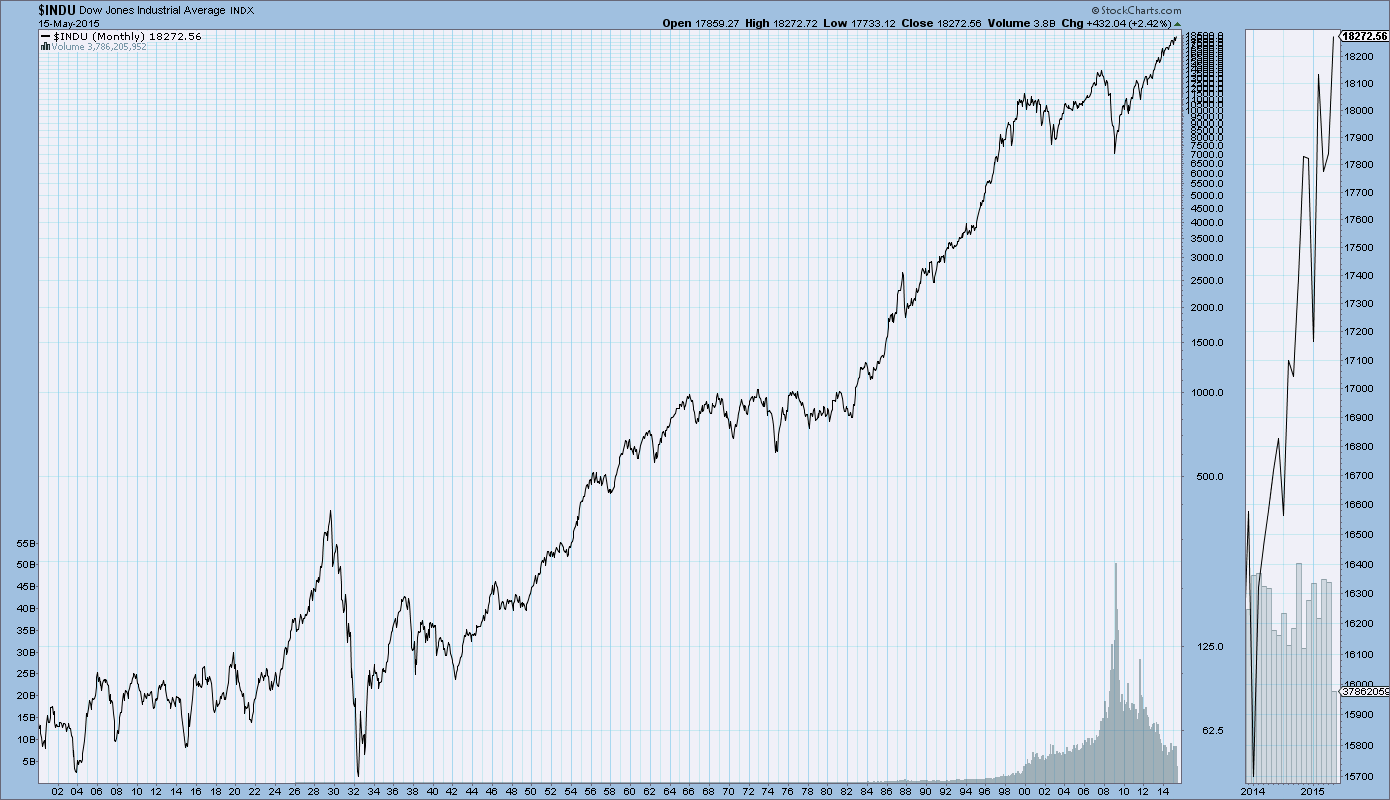

SPX at 2125.85 as this post is written