On May 31, 2017, the Zillow Q2 2017 Home Price Expectations Survey results were released. This survey is done on a quarterly basis.

Two excerpts from the Press Release:

Expectations for overall home price growth are stronger now than they were a year ago. A year ago, panelists predicted that home prices would rise 3.4 percent in 2017. Now, they expect to see a 4.8 percent increase. Their forecasts for home price growth in 2018 are also more optimistic now compared to last year.

also:

"On the heels of last year's nearly seven percent national home value appreciation rate, the prospect that prices will increase less than five percent overall this year might be dispiriting to some," said Pulsenomics founder Terry Loebs. "Yet, 4.8 percent is not only well above the historical average annual gain, it's the most optimistic projection for 2017 that we've seen from our expert panel over the past five years. Although most pessimistic experts still expect a sharp slowdown to commence in 2018, even this group anticipates home values to increase an average of nearly four percent this year. Given these projections, it's a pretty safe bet that U.S. home equity growth will exceed $1 trillion for the sixth consecutive year, and continue to buttress consumer confidence and household spending in 2017, especially if more of today's renters can afford the transition to homeownership."

–

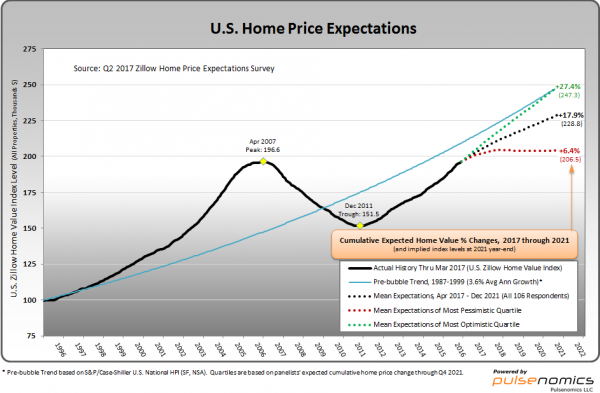

Various Q2 2017 Zillow Home Price Expectations Survey charts are available, including that seen below:

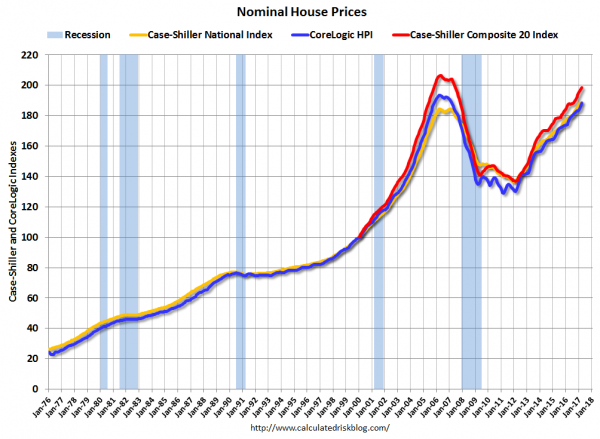

As one can see from the above chart, the average expectation is that the residential real estate market, as depicted by the U.S. Zillow Home Value Index, will continually climb.

The detail of the Q2 2017 Home Price Expectations Survey (pdf) is interesting. Of the 100+ survey respondents, only six (of the displayed responses) forecasts a cumulative price decrease through 2021, and only one of those forecasts is for a double-digit percentage decline. That forecast is from Mark Hanson, who foresees a 24.47% cumulative price decrease through 2021.

The Median Cumulative Home Price Appreciation for years 2017-2021 is seen as 5.00%, 9.22%, 12.49%, 15.69%, and 18.76%, respectively.

For a variety of reasons, I continue to believe that even the most “bearish” of these forecasts (as seen in Mark Hanson’s above-referenced forecast) will prove too optimistic in hindsight. From a longer-term historical perspective, such a decline is very mild in light of the wild excesses that occurred over the “bubble” years.

I have written extensively about the residential real estate situation. For a variety of reasons, it is exceedingly complex. While many people continue to have an optimistic view regarding future residential real estate prices, in my opinion such a view is unsupported on an “all things considered” basis. Furthermore, from these price levels there exists outsized potential for a price decline of severe magnitude, unfortunately. I discussed this downside, based upon historical price activity, in the October 24, 2010 post titled “What’s Ahead For The Housing Market – A Look At The Charts.”

_____

The Special Note summarizes my overall thoughts about our economic situation

SPX at 2408.37 as this post is written