On Wednesday, March 20, 2024 FOMC Chair Jerome Powell gave his scheduled March 2024 FOMC Press Conference. (link of video and related materials)

Below are Jerome Powell’s comments I found most notable – although I don’t necessarily agree with them – in the order they appear in the transcript. These comments are excerpted from the “Transcript of Chair Powell’s Press Conference“ (preliminary)(pdf) of March 20, 2024, with the accompanying “FOMC Statement” and “Summary of Economic Projections” (pdf) dated March 20, 2024.

Excerpts from Chair Powell’s opening comments:

Inflation has eased notably over the past year but remains above our longer-run goal of 2 percent. Estimates based on the Consumer Price Index and other data indicate that total PCE prices rose 2.5 percent over the 12 months ending in February; and that, excluding the volatile food and energy categories, core PCE prices rose 2.8 percent. Longer-term inflation expectations appear to remain well anchored, as reflected in a broad range of surveys of households, businesses, and forecasters, as well as measures from financial markets. The median projection in the SEP for total PCE inflation falls to 2.4 percent this year, 2.2 percent next year, and 2 percent in 2026.

also:

The Fed’s monetary policy actions are guided by our mandate to promote maximum employment and stable prices for the American people. My colleagues and I are acutely aware that high inflation imposes significant hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing, and transportation. We are strongly committed to returning inflation to our 2 percent objective.

The Committee decided at today’s meeting to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent and to continue the process of significantly reducing our securities holdings. As labor market tightness has eased and progress on inflation has continued, the risks to achieving our employment and inflation goals are coming into better balance. We believe that our policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year. The economic outlook is uncertain, however, and we remain highly attentive to inflation risks. We are prepared to maintain the current target range for the federal funds rate for longer, if appropriate.

Excerpts of Jerome Powell’s responses as indicated to various questions:

NICK TIMIRAOS. How much of that inflation that we’ve seen so far this year do you chalk up to one-off calendar adjustment affects following a period of high inflation versus some change in the trend we saw the second half of last year?

CHAIR POWELL. I want to start by being, saying, I always try to be careful about dismissing data that we don’t like. So, you need to check yourself on that and I’ll do that, but so I would say the January number, which was very high, the January CPI and PCE numbers were quite high, there’s reason to think that there could be seasonal affects there. But nonetheless, we don’t want to be completely dismissive of it. The February number was high, higher than expectations, but we have it at currently well below 30 basis points core PCE, which is not terribly high. So it’s not like the January number. But I take the two of them together and I think they haven’t really changed the overall story which is that of inflation moving down gradually on a sometimes-bumpy road toward two percent. I don’t think that story has changed. I also don’t think that those readings added to anyone’s confidence that we’re moving closer to that point, but we didn’t– the last thing I’ll say is we didn’t excessively celebrate the good inflation readings we got in the last seven months of last year. We didn’t take too much signal out of that, what you heard us saying was that we needed to see more that we could, that we wanted to be careful about that decision and we’re not going to overreact as well to these two months of data, nor are we going to ignore them.

also:

CHRIS RUGABER. Hi, Chris Rugaber, the Associated Press. Thank you. In the projections there is an increase in the neutral rate as you know, and higher rates, a quarter point higher rates projected in 2025, 2026. Can you speak about what might be behind that? Is there a real sense here that the economy has perhaps changed in some way that higher rates will be needed in the future? Thank you.

CHAIR POWELL. So, you’re right. They’re pretty midst changes but you’re right, there was an uptick in the longer run rate, and also there’s a 25 basis point increase in ’25 and ’26. In terms of are rates going to be higher in the longer run, if that’s really your question, I don’t think we know that. I think it’s, we think that rates were generally low during the pre-pandemic postglobal financial crisis era, for reasons that are mostly important, slow moving large things like demographics and productivity and that sort of thing. Things that don’t move quickly. But I don’t think we know. I mean my instinct would be that rates will not go back down to the very low levels that we saw where all around the world there were long run rates that were at or below zero in some cases. I don’t see rates going back down to that level, but I think there’s tremendous uncertainty around that.

CHRIS RUGABER. Great, and just a quick follow; on the projections you also have 2.6 percent core inflation for the end of this year. It’s already at, or you mentioned it being 2.8 in February, I mean that doesn’t sound like much disinflation at all. So are you really, are you still confident or, at the last press conference you sounded pretty optimistic you would get more confidence in the end of this year. Is it right to say that this suggests you’re not seeing a lot of disinflation this year compared to what we’ve seen 2023 and so forth?

CHAIR POWELL. I think that that, the higher yearend number reflects the data we’ve seen so far this year. Because you’re now in this year, so I think that– Sorry, say your last part of your question again.

CHRIS RUGABER. Are you still optimistic that you’ll get the confidence you need this year?

CHAIR POWELL. I think if you look at the SEP, what it says is that it is still likely in most people’s view that we will achieve that confidence and that there will be rate cuts. But that’s really going to depend on the incoming data, it is. The other thing is, in the second half of the year you have some pretty low readings so it might be harder to make progress as you move that 12-month window forward. Nonetheless, we’re looking for data that confirm the kind of low readings that we had last year and give us a higher degree of confidence that what we saw was really inflation moving sustainably down to two percent, toward two percent.

also:

NEIL IRWIN. Hi Chair Powell, Neil Irwin with Axios. How do you assess the state of financial conditions right now and particularly, in particular do you view the kind of easing financial conditions since the fall is consistent and compatible with what you’re trying to achieve on the inflation mandate?

CHAIR POWELL. So we think, there are many different financial conditions indicators and you can kind of see different answers to that question. But ultimately, we do think that financial conditions are weighing on economic activity and we think you see that in, a great place to see it is in the labor market where you’ve seen demand cooling off a little bit from the extremely high levels and there I would point to job openings, quits, surveys, the hiring rate, things like that are really demand. There are also supply-side things happening, but I think those are demand side things happening. We saw, that’s been a question for a while, we did see progress on inflation last year, significant progress despite financial conditions sometimes being tighter, sometimes looser.

_____

_____

The Special Note summarizes my overall thoughts about our economic situation

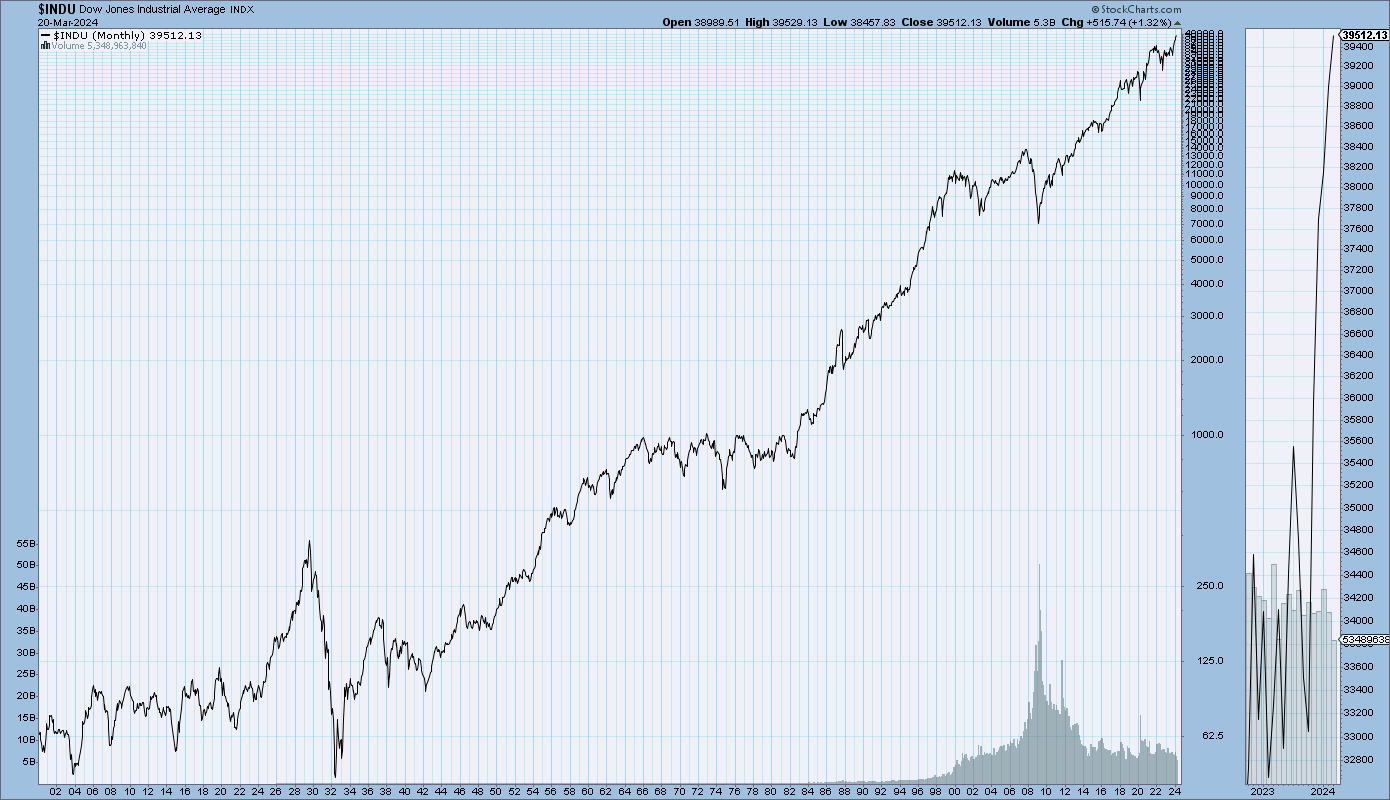

SPX at 5246.65 as this post is written