I view Walmart’s results and comments as particularly noteworthy given their retail prominence and focus on low prices. I have previously commented on their quarterly management call comments; these previous posts are found under the “

paycheck to paycheck” label.

Here are various excerpts that I find most notable:

comments from Doug McMillon, President and CEO, page 3:

As we expected, operating income continued to be pressured by our decision to invest in our front line associates. To improve the store experience for our customers and create a bridge to our future where digital capabilities will play an increasing role in our stores, we’re making a $1.2 billion planned investment in our people this year that we understood would impact near-term operating income. This is by far the biggest driver of the decline in consolidated operating income.

comments from Claire Babineaux-Fontenot, EVP and treasurer, page 9:

I’ll close today’s discussion with a few comments on returns. At Walmart, we remain committed to providing good returns for our shareholders. During last month’s meeting for the investment community, we announced a new share repurchase authorization of $20 billion, and said that our intention is to utilize this authorization over a two-year period. The company repurchased approximately 6.1 million shares for $437 million during the third quarter.

comments from Greg Foran, president and CEO of Walmart U.S., page 10:

Our customers told us they’re happy with the improvements we’re making in their shopping experience, as reflected in our customer experience scores. To date, 70 percent of our stores have achieved the initial goal we set for them, and we’ll raise the bar for next year. We also saw some progress this quarter in gross margin, with the work we’ve put in on pharmacy, markdowns, and shrink. However, as we’ve discussed before, the investments in our stores and our associates are significant, and will continue to pressure the bottom line.

comments from Greg Foran, president and CEO of Walmart U.S., page 12:

Moving on to the remainder of our financials…gross margin increased 32 basis points versus last year. Gross margin rate improved in food, general merchandise, and consumables but was somewhat offset by declines in health & wellness. Reimbursement levels continued to pressure pharmacy profits; however, we’ve made some strides across several initiatives that improved margins in this department versus Q2. Additionally, we remained focused on our urgent agenda items, including better management of markdowns to zero. Finally, while only just beginning to show in our results, we are pleased with our efforts thus far on addressing shrink, which has been a significant headwind for us this year.

_____

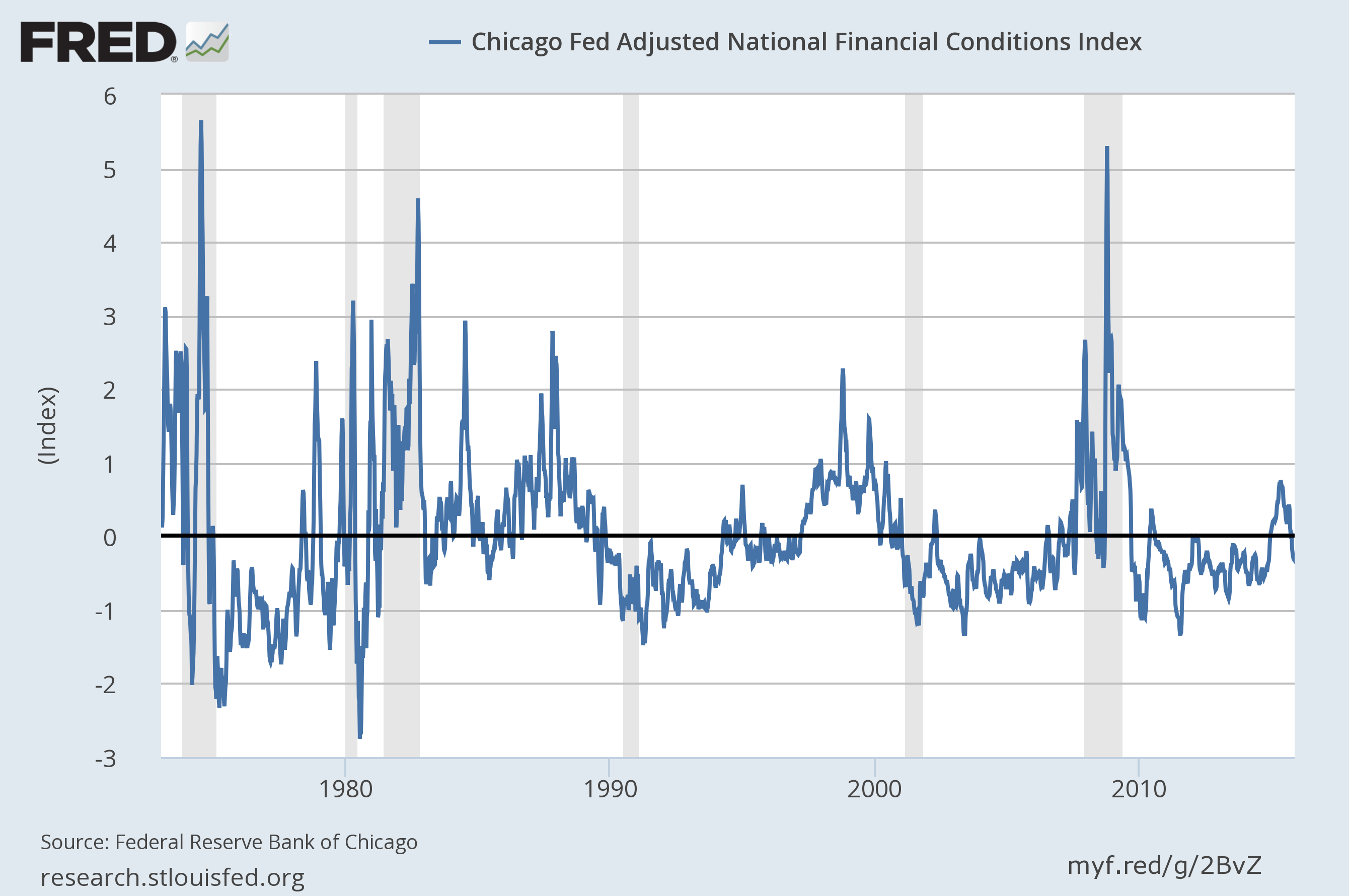

The Special Note summarizes my overall thoughts about our economic situation

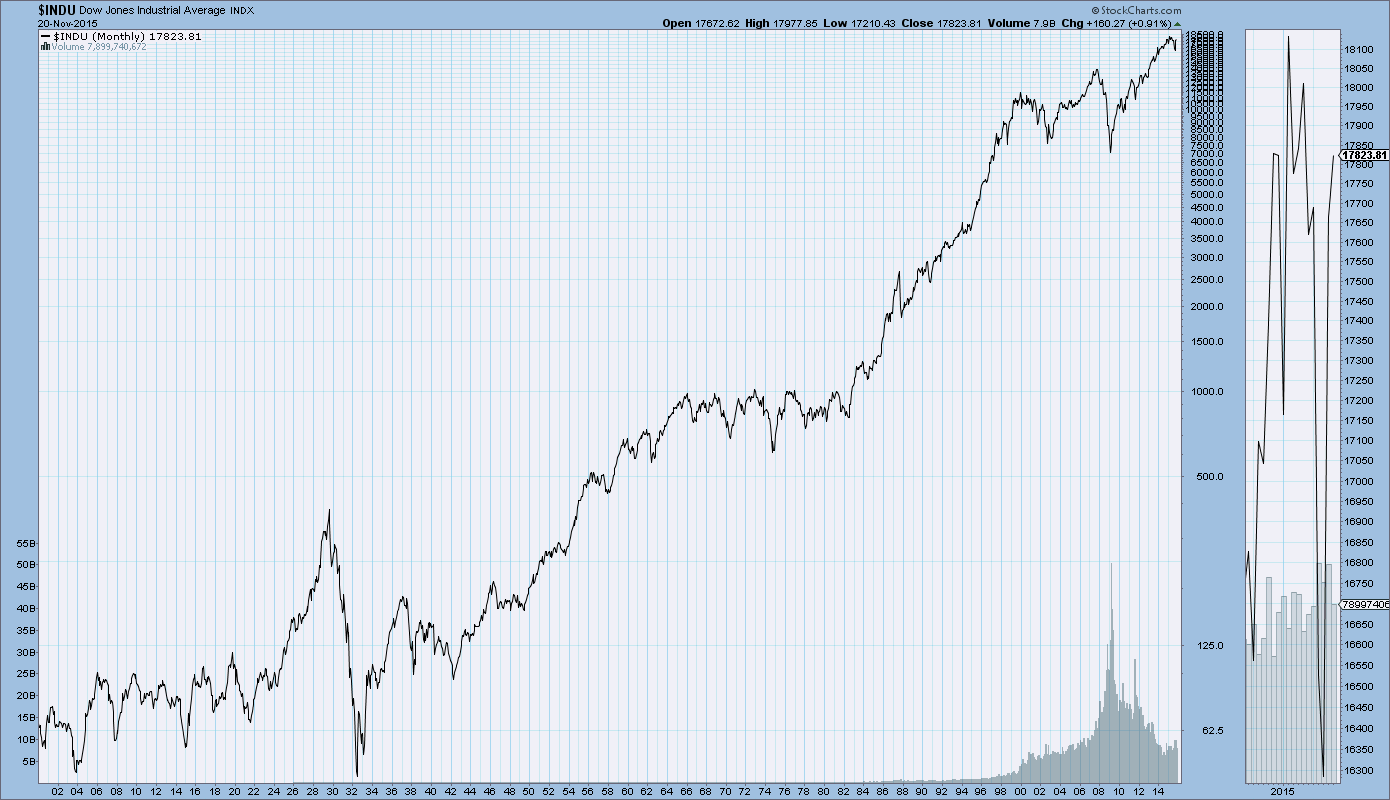

SPX at 2054.61 as this post is written