On Wednesday, June 14, 2017 Janet Yellen gave her scheduled

June 2017 FOMC Press Conference. (link of video and related materials)

Below are Janet Yellen’s comments I found most notable – although I don’t necessarily agree with them – in the order they appear in the transcript. These comments are excerpted from the “

Transcript of Chairman Yellen’s Press Conference“ (preliminary)(pdf) of June 14, 2017, with the accompanying “

FOMC Statement” and “

Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, June 2017“ (pdf).

From Janet Yellen’s opening comments:

Following a slowdown in the first quarter, economic growth appears to have rebounded,

resulting in a moderate pace of growth so far this year. Household spending, which was

particularly soft earlier this year, has been supported by solid fundamentals, including ongoing improvement in the job market and relatively high levels of consumer sentiment and wealth.

Business investment, which was weak for much of last year, has continued to expand. And

exports have shown greater strength this year, in part reflecting a pickup in global growth.

Overall, we continue to expect that the economy will expand at a moderate pace over the next

few years.

In the labor market, job gains have averaged about 160,000 per month since the start of

the year--a solid rate of growth that, although a little slower than last year, remains well above estimates of the pace necessary to absorb new entrants to the labor force. The unemployment rate has fallen about 1/2 percentage point since the beginning of the year and was 4.3 percent in May, a low level by historical standards and modestly below the median of FOMC participants’ estimates of its longer-run normal level. Broader measures of labor market utilization have also improved this year. Participation in the labor force has been little changed, on net, for about three years. Given the underlying downward trend in participation stemming largely from the aging of the U.S. population, a relatively steady participation rate is a further sign of improving conditions in the labor market. Looking ahead, we expect that the job market will strengthen somewhat further.

Janet Yellen’s responses as indicated to the various questions:

SAM FLEMING. Thank you very much. Sam Fleming from the Financial Times. We've

now had a very long streak of-- or fairly long streak of weak inflation numbers at least measured by the CPI this morning as well. Marketplace-based inflation expectations are declining. What kind of vigilance are you now saying is needed in terms of weak inflation? How does that interact with your policy outlook? And would further disappointments argue for pressing pause on rate hikes or delaying balance sheet run-off? How do you think about those two potential responses to weak inflation?

CHAIR YELLEN. So, let me just say as I emphasized in my statement and always say monitory policy is not on a preset course. We indicated in our statement today that we're closely

monitoring inflation developments and certainly have taken note of the fact there have been

several weak readings particular on core inflation. Our statement indicates that we expect

inflation to remain low in the near term. But on the other hand, we continue to feel that with a

strong labor market and labor market that's continuing to strengthen, the conditions are in place for inflation to move up. Now, obviously we need to monitor that very carefully. And ensure especially with roughly five years of inflation running under our 2 percent objective that is a goal to which the committee is strongly committed. And we need to make sure that we have in place the policies that are necessary to achieve 2 percent inflation and I pledge that we will do that. But let me say with respect to recent readings, it's important not overreact to a few readings and data on inflation can be noisy. As I pointed out, there have been some idiosyncratic factors I think that have held down inflation in recent months, particularly a huge decline in cell telephone service plan prices, some declines in prescription drugs. We had an exceptionally low reading on core PC in March, and that will continue to hold down 12-month changes until that reading drops out. But we are this morning's reading on the CPI showed weakness in a number of categories and it's certainly something that we will be closely monitoring in the months ahead. We will--we're focused on in making our policy decisions on the medium term outlook and we will, you know, be looking carefully at incoming data and as always revising our outlook and policy plans as appropriate.

also:

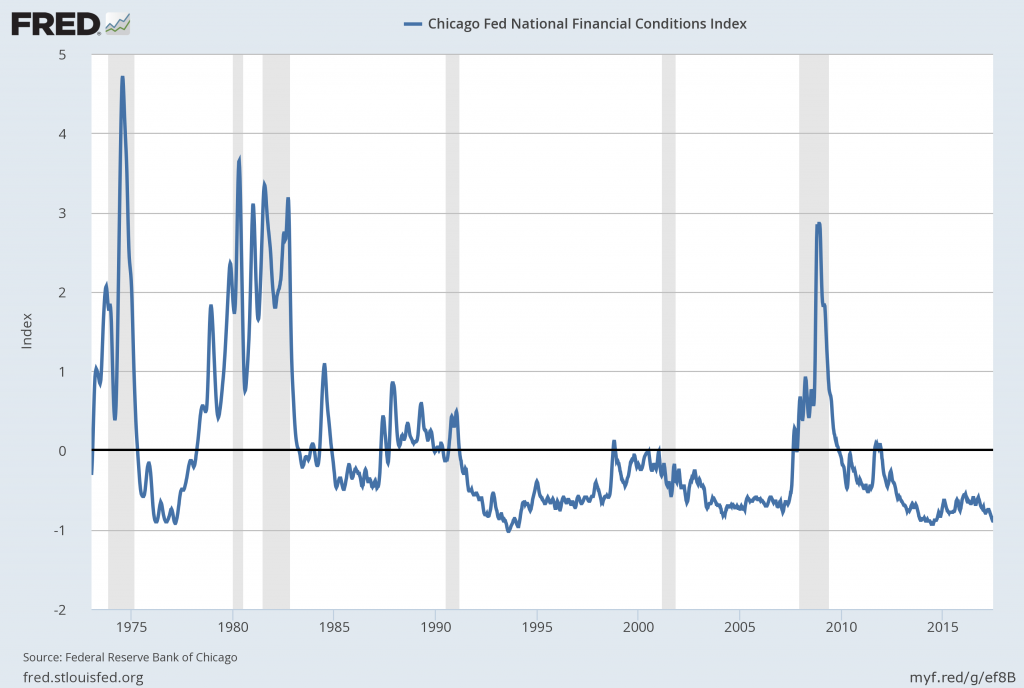

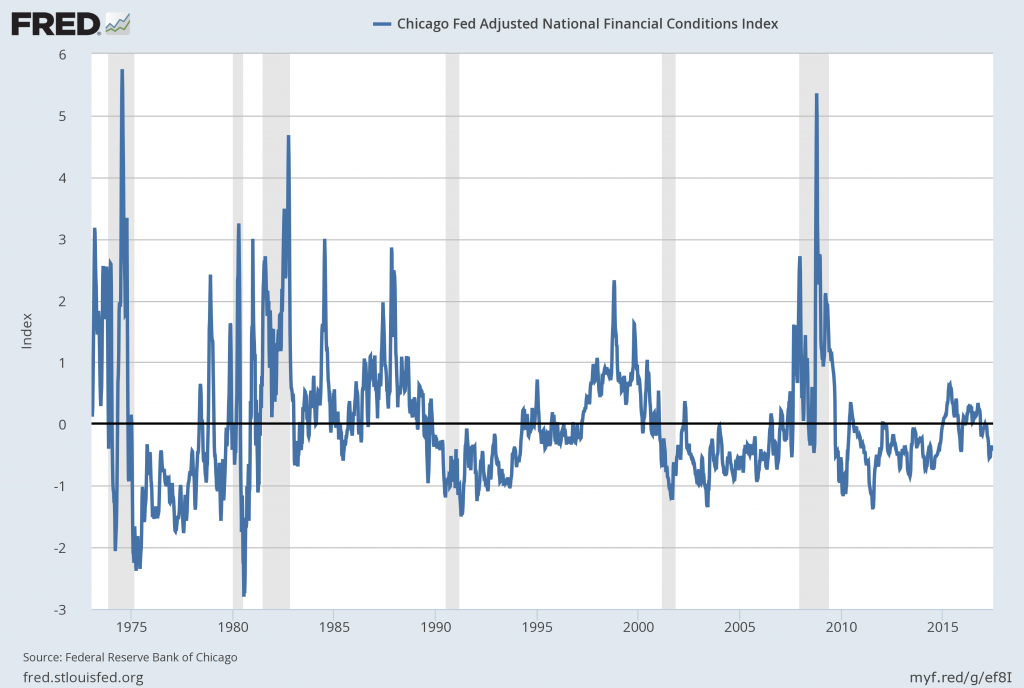

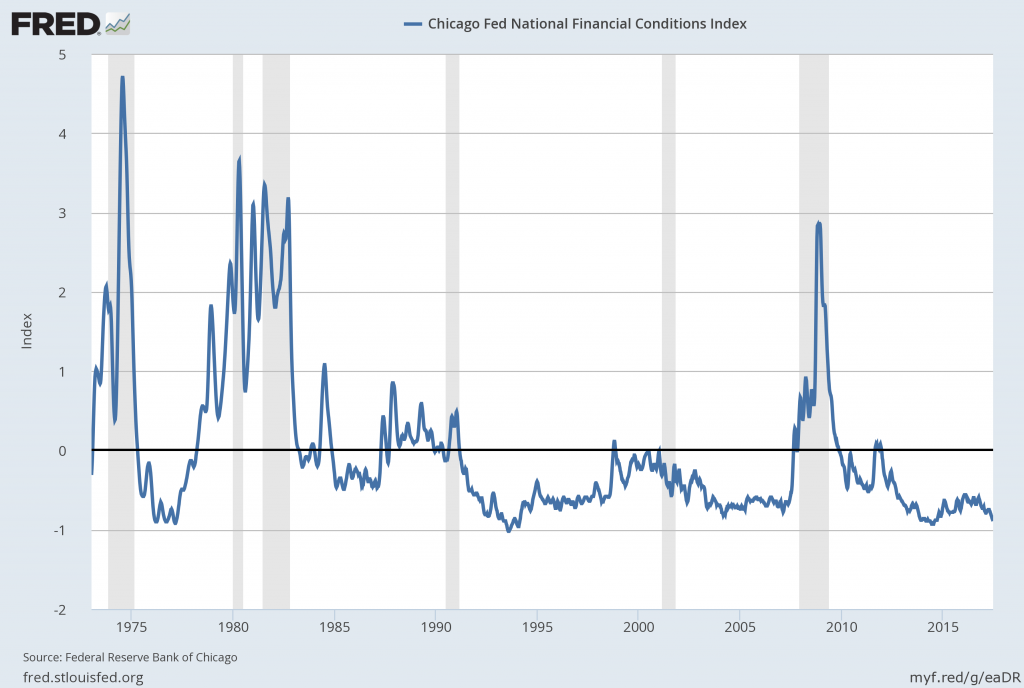

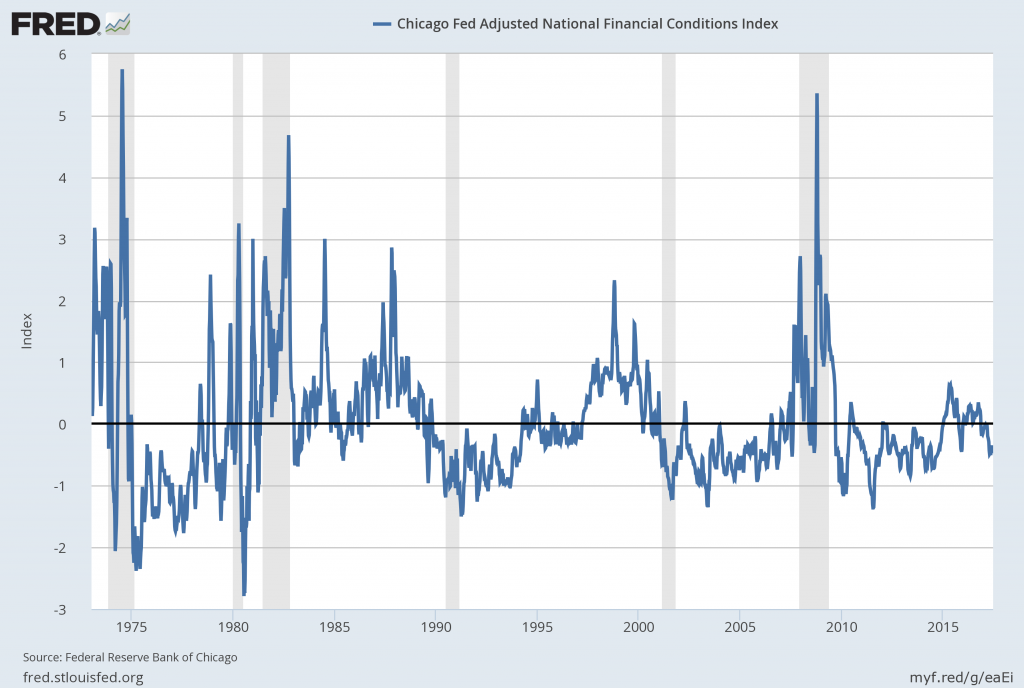

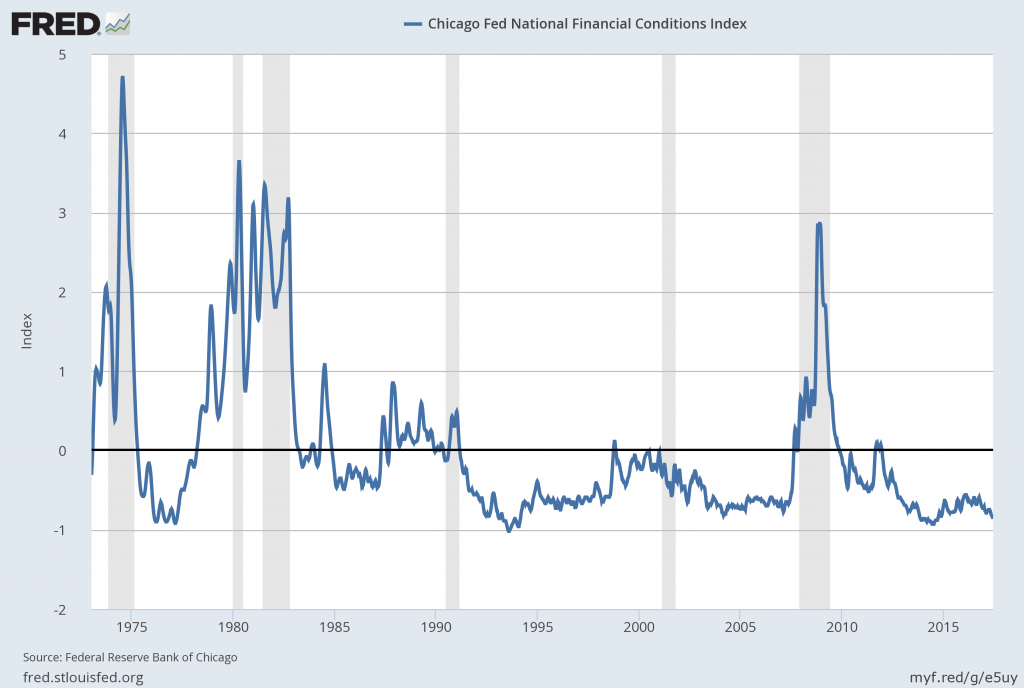

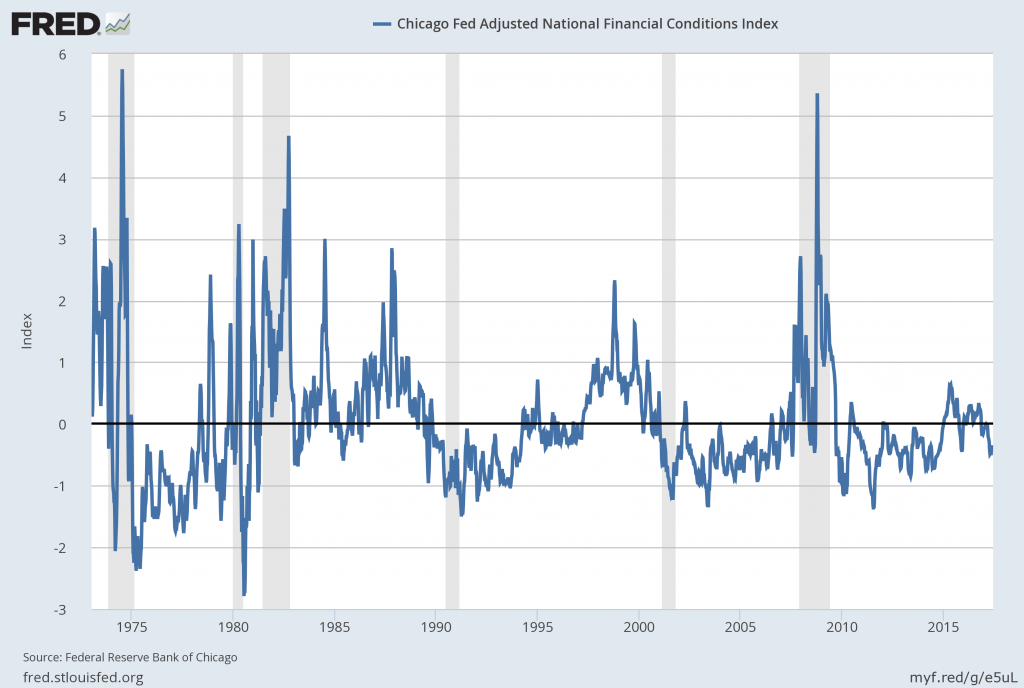

BINYAMIN APPELBAUM. Binyamin Appelbaum, the New York Times. Measures of financial conditions show that since the Fed started raising interest rates two years ago, financial conditions actually have loosened. Consumer business borrowing costs in many cases are down. Do you have the sense that the market is not listening to you? How much of a concern is that for you? And at some point, does it convince you that you need to raise rates perhaps more quickly?

CHAIR YELLEN. Well, in deciding what the appropriate path of rates is, we take many

different factors into account. We have certainly noticed the stock market is up considerably over the last year. That usually shows up in financial conditions indexes and is an important reason why some of them show easier financial conditions. There has been a modest decrease recently in the value of the dollar although it's up substantially since mid-2014. So, we take those factors into account in deriving our forecasts and deciding the appropriate stance of policy. We have done that and-- but other things also affect the stance of policy. So there really can't be any simple relationship. We're not targeting financial conditions. We're trying to set a path of the federal funds rate, the taking into account of those factors and others that don't show up in the financial conditions index. We're trying to generate paths for employment and inflation that meet our mandated objectives.

also:

NANCY MARSHALL-GENZER. Hi, Nancy Marshall-Genzer from Marketplace. Recently, a group of economists send the Fed a letter earlier this month, disagreeing with your 2 percent inflation target and saying, they would like the economy to run a bit hotter. They don't think the labor market is so tight. You say you're committed to the 2 percent target, but what do you say to them?

CHAIR YELLEN. So, at the time that we adopted the 2 percent target, it was back in

2012, we had a very thorough discussion of the factors that should determine what our inflation objective should be. And, you know, I believe that was a well thought out decision. Now, at the moment, we are highly focused on trying to achieve our 2 percent objective. And we recognize the fact that inflation has been running below and it's essential for us to move inflation back to that objective. Now, we've learned a lot in the meantime and assessments of the level of the neutral likely level currently and going forward of the neutral federal funds rate have changed and are quite a bit lower than they stood in 2012 or earlier years. And that means that the economy is-- has the potential where policy could be constrained by the zero lower bound more frequently than at the time that we adopted our 2 percent objective. So, it's that recognition that causes people to think we might be better off with a higher inflation objective, and that's an important set. This is one of our most critical decisions and one we are attentive to evidence and outside thinking. It's one that we will be reconsidering at some future time. And it's important for our decisions to be informed by a wide range of views and research which is ongoing inside and outside the Fed. But a reconsideration of that objective needs to take account, not only of benefits of a higher in potential benefits, of a higher inflation target, but also the potential cost that could be associated with it. It needs to be a balanced assessment. But I would say that this is one of the most important questions facing monetary policy around the world in the future and we very much look forward to seeing research by economists that will help inform our future decisions on this.

also:

MICHAEL MCKEE. And the characterization of you as a low-interest rate person?

CHAIR YELLEN. Well, I have felt that it's been appropriate for interest rates to remain

low for a very long time. We are in the process of as the economy strengthens normalizing

interest rates. But certainly, we've had a lot of years in which interest rates have been low. I

thought it was necessary to support the economy at that time and was strongly in favor of those policies.

also:

MICHAEL DERBY. Mike Derby from Dow Jones Newswires. In light of the plans to trim the balance sheet hopefully later this year, what have you learned about QE and your bond

buying policies as a tool for monetary policy? When they were launched, it wasn't something

you had, you know, engaged in that scale before, a lot of fear and said it was going to create a

hyperinflation that hasn't ever seem to come to pass. So, you know, in light of QE as potentially

a tool for the future, you know, it might come back again, what have you learned about how it

works in the economy? Like where do you see it affect things? You know, what are sort of the

lessons learned of the experience?

CHAIR YELLEN. Well, thanks. That's a great question. I mean, staff in the Federal Reserve and outside economists who have done a great deal of work trying to evaluate QE, I think the general conclusion is that it has worked in that it has put some downward pressure on

longer term interest rates, so-called term premiums embedded in longer term interest rates.

There's disagreement among economists about exactly how large those effects are and it's

something that's difficult to pin down. But obviously, it has not caused runaway inflation quite

the contrary. I mean, that was never my expectation but I do remember when people were afraid that that would happen. We do have the tools. We have, you know, even with a large balance sheet, we intend to shrink our balance sheet now. But even with a large balance sheet, we retain the ability to move the fed funds rate and set it as appropriate to the needs of the economy. So, I think we have learned that it works. It's a valuable part of the toolkit. It's something that if we were to encounter an episode in the future of extreme weakness where I've said, we want the fed funds rate and movements in short-term interest rates, that's our go-to number one main policy tool. But if we were to hit the zero lower bound and constrained in our use of that tool, certainly balance sheet policies and forward guidance of the type that we provided, I believe based on the evidence of how they worked or to remain part of our toolkit. And we have said in the bullets that we released today on our balance sheet that in such of-- an episode of such extreme weakness in the future, those are things we would consider going forward.

MICHAEL DERBY. One small follow-up. Is four and a half trillion sort of a natural limit

to how high you might want to push the balance sheet or could you envision it going higher if

you needed it to?

CHAIR YELLEN. Well, we've had no discussion of that issue, you know. And our focus

now is on getting it back to a more normal size. But I would say the use of QE in the United

States relative to the size of our economy is not as high as it's been in some other countries that

have employed it. But that's something we haven't seriously even discussed.

_____

The Special Note summarizes my overall thoughts about our economic situation

SPX at 2432.46 as this post is written