Recently Deloitte released their “CFO Signals” “High-Level Summary” report for the 2nd Quarter of 2019.

As seen in page 2 of the report, there were 159 survey respondents. As stated:

“Each quarter (since 2Q10), CFO Signals has tracked the thinking and actions of CFOs representing many of North America’s largest and most influential companies.

All respondents are CFOs from the US, Canada, and Mexico, and the vast majority are from companies with more than $1 billion in annual revenue. For a summary of this quarter’s response demographics, please see the sidebars and charts on this page. For other information about participation and methodology, please contact nacfosurvey@deloitte.com.”

Here are some of the excerpts that I found notable:

from page 3:

Perceptions

How do you regard the status of the North American, European, and Chinese economies? Perceptions of North America declined slightly, with 79% of CFOs rating current conditions as good (down from 80% last quarter), and 24% expecting better conditions in a year (down from 28%). Perceptions of Europe slid to just 10% and 4%; China sits at 26% and 10%. Page 6.

What is your perception of the capital markets? Seventy-seven percent of CFOs say debt financing is attractive (up from 70%). Equity financing attractiveness rose for both public (from 25% to 40%) and private (27% to 35%) company CFOs. Sixty-four percent say US equity markets are overvalued, up from 46% and similar to the levels from 2018. Page 7.

Sentiment

What external/internal risks worry you the most? CFOs express strong concerns about the impact of US trade policy on global growth and about US political turmoil. Talent is the dominant internal concern, with newly emerging concerns about rising labor costs. Page 8.

Compared to three months ago, how do you feel about the financial prospects for your company? The net optimism index declined from last quarter’s +16 to just +9 this quarter—the second-lowest reading in three years. Thirty percent of CFOs express rising optimism (32% last quarter), and 21% express declining optimism (16% last quarter). Page 9.

Expectations

What is your company’s business focus for the next year? CFOs indicate a bias toward revenue growth over cost reduction (48% vs. 29%), investing cash over returning it (51% vs. 18%), current offerings over new ones (47% vs. 32%), and current geographies over new ones (66% vs. 13%). Page 10.

How do you expect your key operating metrics to change over the next 12 months? YOY revenue growth expectations fell from 4.8% to 3.8%, earnings growth slid from 7.1% to 6.1%, and hiring fell from 2.1% to 1.9% (all sit at twoyear lows). Dividend growth declined from 3.9% to 3.7%, the lowest level in two years. Capital spending rose substantially from 5.9% to 7.7%. Page 11.

Special topic: Company growth, profitability, and investment

If the US experiences a pullback, what type of pullback do you expect? About 80% expect a downturn to be mild, and they are split on whether that downturn will be short or prolonged. Pages 12.

What industry and company factors are affecting your business planning? All industries expected rising industry revenue over declining, with Manufacturing lowest and Healthcare/Pharma highest. All industries except Technology and Retail/Wholesale claimed to be in profitability mode over growth mode; all except Financial Services were biased toward market expansion over consolidation. Overall, companies claimed substantial talent constraints, but not capital constraints or shareholder pressure to use/return cash. Page 13.

What are your company’s top uses of cash this year? Top uses revolve around investment for growth and productivity improvement. There are substantial public/private and industry differences when it comes to returning cash, paying down debt, and investing for growth versus for productivity. Page 14.

Which markets will be important to your company’s growth over the next five years? Predictably, CFOs ranked their home markets most important. The US ranked universally high, but the importance of Canada and Mexico to US CFOs seems to have declined since we last asked in 4Q15; China is the most important market outside North America on the whole. Page 15.

What is your approach to growth investments over the next three years? The vast majority of CFOs say they are making focused growth investments instead of spreading investments across multiple opportunities; capital-constrained companies are the most likely to be avoiding major investment. Page 16.

On which areas will you personally focus for the next year? Three areas comprise the top tier for CFOs’ personal focus: profitability, corporate strategy, and growth. Other focus areas were substantial for particular industries. Page 17.

from page 9:

Sentiment

Optimism regarding own-companies’ prospects

Own-company optimism continues to sit among its lowest levels in the last three years. The US is highest at just +15; Canada and Mexico are both overwhelmingly negative.

Last quarter’s net optimism rebounded somewhat from the prior quarter’s three-year low of +3 to a modest +16. This quarter it retreated to +9 and sits at the second-lowest reading in three years. Thirty percent of CFOs expressed rising optimism (down from 32%), and 21% cited declining optimism (up from 16%).

Net optimism for the US declined from last quarter’s +19 to +15, the second-lowest level in the last three years. Canada fell sharply from last quarter’s +25 to -25. Mexico rose from last quarter’s dismal -60 to a still-poor 43, tying the second lowest point in the last two years.

Manufacturing, Retail/Wholesale, and Healthcare/Pharma were comparatively pessimistic (+2, +6, and -27, respectively). Technology was strongest at +20, with Financial Services and Energy/Resources slightly behind at +15.

Please see the full report for industry-specific charts. Note that industry sample sizes vary markedly and that the means are most volatile for the least-represented. Due to a very small sample size, T/M/E was not used as a comparison point this quarter.

from page 11:

Expectations

Growth in key metrics, year-over-year

Expectations for revenue, earnings, dividends, hiring, and wages all declined to their lowest levels in the last two years; capital spending rose but remains below the two-year average.

Revenue growth declined from 4.8% to 3.8%, its lowest level since 4Q16. The US slid to a twoyear low. Canada dipped slightly, and remained below its two-year average. Mexico declined to a two-year low. Technology and Energy/Resources again lead; Healthcare/Pharma trails.

Earnings growth declined from 7.1% to 6.1%, the lowest level since 3Q16. The US fell to a twoyear low. Canada fell and remains below its twoyear average. Mexico dipped and remained below its two-year average. Retail/Wholesale is highest; Manufacturing and Healthcare/Pharma are lowest.

Capital spending growth rose substantially from 5.9% to 7.7%, just below the two-year average. The US rose to just above its two-year average. Canada and Mexico declined and sit below their two-year averages. Healthcare/Pharma and Retail/Wholesale are again highest; Services is lowest.

Domestic personnel growth slid from 2.1% to 1.9%, the lowest level since 3Q16. The US fell to its lowest level in more than two years. Canada slid below its two-year average. Mexico rose, but remains below its two-year average. Services and Technology lead; Energy/Resources trails.

Dividend growth declined from 3.9% to 3.7, the lowest level in two years.

Please see the full report for industry-specific charts. Note that industry sample sizes vary markedly and that the means are most volatile for the least-represented. Due to a very small sample size, T/M/E was not used as a comparison point this quarter.

–

Among the various charts and graphics in the report are graphics depicting trends in “Own Company Optimism” on page 9 and “Economic Optimism” found on page 6.

_____

I post various business and economic surveys because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with many of the consensus estimates and much of the commentary in these surveys.

_____

The Special Note summarizes my overall thoughts about our economic situation

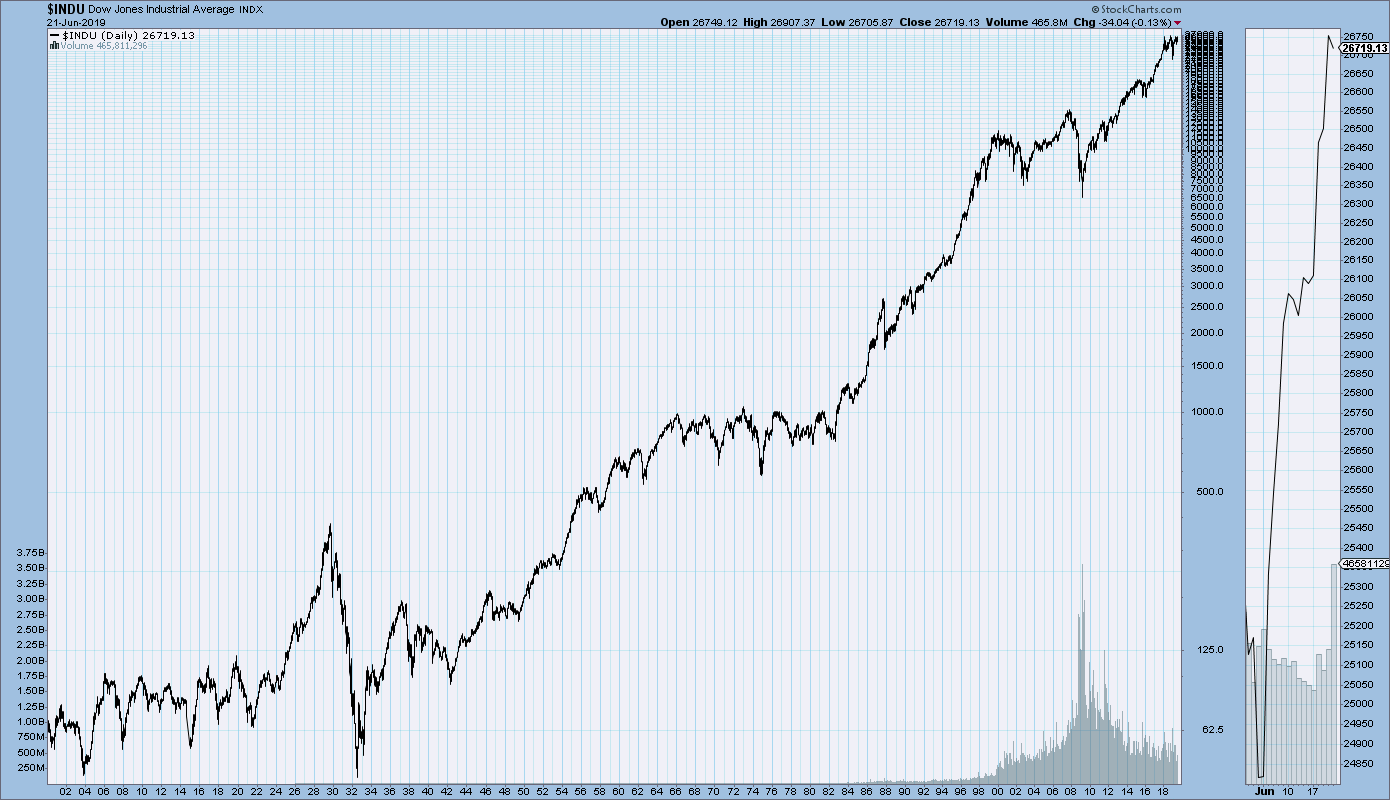

SPX at 2926.46 as this post is written