From Janet Yellen’s opening comments:

The Committee continues to see sufficient underlying strength in the economy to support ongoing improvement in the labor market. Real GDP looks to have increased robustly in the third quarter, reflecting solid consumption and investment spending. Smoothing through the quarterly ups and downs earlier this year, real GDP expanded around 2½ percent over the four quarters ending in the third quarter, and the available indicators suggest that economic growth is running at roughly that pace in the current quarter. The Committee continues to expect a moderate pace of growth going forward.

Inflation has continued to run below the Committee’s 2 percent objective, and the recent sizable declines in oil prices will likely hold down overall inflation in the near term. But as the effects of these oil price declines and other transitory factors dissipate, and as resource utilization continues to rise, the Committee expects inflation to move gradually back toward its objective. In making this forecast, the Committee is mindful of the recent declines in market-based measures of inflation compensation. At this point, the Committee views these movements as likely to prove transitory, and survey-based measures of longer-term inflation expectations have remained stable. That said, developments in this area obviously bear close watching.

Janet Yellen’s responses as indicated to the various questions:

STEVE LIESMAN. Was there concern -- Steve Liesman, CNBC -- was there concern expressed at the meeting that the signal coming from markets -- and a variety of markets -- lower oil prices? Lower yields around the world, was one of deflation, and that that risk was one that should perhaps over shadow the concern about inflation on the other side?

CHAIR YELLEN. Well thanks Steve. We're very attentive to global developments. And certainly discuss them in the meeting. The very substantial decline we have seen in oil prices is one of the most important developments shaping the global outlook. It will have different effects in different regions, and could well have effects on financial markets, as we are seeing. I think the judgment of the committee is that from the standpoint of the United States and the U.S. outlook, that the decline we have seen in oil prices is likely to be on net; a positive. It's something that's certainly good for families, for households. It's putting more money in their pockets. Having to spend less on gas and energy, and so in that sense, it's like a tax cut that boosts their spending power. The United States remains -- although our production of oil has increased dramatically -- we still remain a net importer of oil. Of course there may be some offset in the form of reduced drilling activity, and possibly some change, some reduction in CAPEX plans in the drilling area. But on balance, I would see these developments as a positive for the standpoint of the U.S. economy. With respect to deflation, we see downward pressure on headline inflation from declining energy prices. We certainly recognize that that is going to be pushing down headline inflation. And may even spill over to some extent to core inflation. But at this point, although we indicated we're monitoring inflation developments carefully, we see these developments as transitory. And the committee continues to believe -- especially with the improvement we're seeing in the labor market -- which we expect to continue -- that inflation will move back up to our 2 percent objective over time. As I indicated, we will want to feel, I believe, that people will expect to feel reasonably confident about that when they -- when the process of normalization begins. But we do expect them to be transitory.

also:

STEVEN MUFSON. Hi. Steve Mufson from The Washington Post. I was just hoping you could go into a little more detail about the oil effect. Even though you see it as transitory, does that give you a little more room to keep rates low in the next few months? And if -- alternately, if prices bounce back, what's that going to do to your ability to changes rates, and how might you react to that?

CHAIR YELLEN. Well I -- I'd say, you know, that I think what we have seen since the mid-80s is that in an environment where inflation expectations are well-anchored, that movements in oil, and commodity prices, and import prices tend to have transitory effects on the inflation outlook. There were many years in which we had unanticipated increases in oil prices. Really, beginning in 2004 and 2005 that put upward pressure on headline inflation and sometimes even spilled through into core, and typically, the committee looked through those impacts on inflation with the view that they would be transitory. And I think, experience bears out that they were transitory. And I think that's the committee’s expectation here. Inflation, even core inflation, has been running below our inflation objective. Movements in oil, you know, are now down and perhaps later up, will move inflation around, certainly headline inflation. But the committee at this point anticipates those impacts to be transitory. So as long as participants feel reasonably confident that the inflation projection is one where we expect to meet our 2 percent objective over time. That's what I think they'll be looking at things as we decide on the path for the funds rate.

also:

PEDRO DA COSTA. Pedro Da Costa with Dow Jones Newswires. Enough about rates. I want to ask you about the New York Fed. The New York Fed's been in the news a lot lately. President Dudley was invited to Congress to testify about conflicts of interest there. You had things like the Segarra tapes, the Beim report, and most recently the revelation that a former New York Fed official was exchanging information with someone at Goldman Sachs who was also-had New York Fed connections. I just wonder--and also there was scandals during the crisis related to Stephen Freidman regarding the New York Fed, and his purchase of Goldman Sachs stock. Do you see the New York Fed as a black mark on the Fed system because of these recurring scandals? Have you talked to Bill Dudley about reforming the image of that particular regional Fed? And do you think a person that has--that spent 21 years of his career at Goldman Sachs is in a position to regain public credibility about conflicts of interest?

CHAIR YELLEN. Well, let me say that I think it's very important for the Federal Reserve System to have confidence in the quality of its supervision. And I do have--I have a good deal of confidence in the quality of our supervision program, for the banking organizations, we supervise in general, and that also applies to the largest banking organizations. We rely on examiners who are in the field and at the Reserve banks to be providing information about what's happening in those organizations. But that information feeds into a process in which it is not individuals at any single Reserve bank. But at the Board, it's a Board-led process, and it involves senior officials at a number of different Reserve banks. It's also a multi-disciplinary process that involves not only people from supervision, but those from markets, from economic research, experts who focus on financial stability all come together to evaluate the information that they have, and to assign supervisory ratings and decide on the appropriate program for all of those large institutions. We've strengthened the process of supervision enormously since the crisis, and I feel a very good sense of confidence in how we're carrying that out.

Now it is important to make sure that we have fed into the--this process. All the information that's relevant to making the right decisions. And when there are individuals who are examiners, who may disagree with others in their team about how to interpret what's going on at a particular institution, it's important that there be channels by which they can make sure that disagreements are fed up to the highest levels. This is true throughout the work we do. We do economic forecasting, and our--the FOMC receives information to help us make decisions. But obviously there are disagreements about--among economists about how to interpret developments. It's also important for us there to make sure we understand alternative views. So this is important in supervision. We've announced that the Board has undertaken a review of whether or not there are appropriate mechanisms in place in all of the Reserve banks that individuals who disagree with decisions can make those--make their own views known, and feed into the process, and we've also asked our inspector general to look into.

also:

GREG ROBB. There's a contagion risk to the--from low oil prices that people are talking about in the markets. What does it mean to the banks that have lent, you know, into the oil patch with the low oil prices? And I guess, you know, your warnings about leverage loans. You have made warnings over the past year about leveraged lending. Are you worried that they haven't been heeded? Thank you.

CHAIR YELLEN. So I mean there is some--you're talking about in the United States exposure? I mean we have seen some impacts of lower oil prices on the spreads for high-yield bonds, where there's exposure to oil companies that may see distress or a decline in their earnings, and we have seen some increase in spreads on high-yield bonds more generally. I think for the banking system as a whole the exposure to oil, I'm not aware of significant issues there.

This is the kind of thing that is part of risk management for banking organizations and the kind of thing they look at in stress tests. But the movements in oil prices have been very large, and undoubtedly unexpected.

We--in terms of leverage, and whether or not levered entities could be badly effected by movements in oil prices, leverage in the financial system in general is way down from the levels before the crisis. So it's not a major concern that there are levered entities that would be badly affected by this, but we'll have to watch carefully. There have been large and unexpected movements in oil prices.

also:

STEVE BECKNER. Good afternoon, Chair Yellen. Steve Beckner of MNI. I will go back to interest rates if you don't mind. Actually it's a question about balance sheet effects on the overall appropriate level of monetary policy. In reaffirming the reinvestment policy, the FOMC says once again that this will help maintain accommodative financial conditions. In the past it's said that the large portfolio securities will exert a downward effect on long-term interest rates. As you look forward to raising short-term rates, to what extent does the FOMC need to take into account this sort of residual, accommodative effect of maintaining a large balance sheet?

CHAIR YELLEN. So I agree, and that's why we stated it that we typically think of the monetary policy impact of our asset purchases as depending on the stock of assets that we hold on our balance sheet, rather than the flow of purchases, and so we're reminding the public that we continue to hold a large stock of assets, and that is tending to push down term premiums in longer-term yields. We made clear when we--or tried to make clear when we issued our normalization principals in September that we intend to use changes in our target for the federal funds rate as the main tool that we will actively use to adjust financial conditions. Rather than actively planning to sell the assets that we've put onto our balance sheet, some time after we begin raising our targets for short-term interest rates, depending on economic and financial conditions, we're likely to reduce or cease reinvestment and gradually run down the stock of our assets. But our active tool for adjusting monetary--the stance of monetary policy so that it is appropriate for the economic needs for the country, that will be done through adjusting our shortterm target range for the federal funds rate.

also:

KEVIN HALL. Kevin Hall with McClatchy Newspapers. I can't believe no one's asked you the most important question about what's going on with your San Francisco 49ers, since everybody's already wished you a happy holiday.

Can you talk a little bit about housing? Few things are more important to Americans in their wealth creation than housing. You've, in your statement, noted that it continues to be a drag. Mr. Dudley has--was actually relatively upbeat in his forecast. I don't know if that's a view shared on the Committee. What do you think is holding housing back? What can Congress do? What will you tell Congress in the coming year? And more--and a clarification on the Dudley question from earlier. You didn't mention him by name in your being pleased by quality of supervision. Are you pleased with Mr. Dudley's handling of the events?

CHAIR YELLEN. So let me start with that. I have great confidence in President Dudley. He's done a fine job in running the New York Fed, and I want to be very clear that I have great confidence in him. He's a distinguished public servant, and he has worked very hard in the aftermath of the crisis to make sure that the New York Fed is doing all that it needs to do to contribute to the work that we do both in the financial stability and in supervision. And let's see, the other question that you asked about was about--

KEVIN HALL. Housing.

CHAIR YELLEN. --about housing. So, you know, I've been surprised that housing hasn't recovered more robustly than it has. In part I think it reflects very tight credit -- continuing tight credit conditions for any borrower that doesn't have really pristine credit, you know, credit ratings, and my hope is that that situation will ease over time. In addition, household formation has been very depressed, and my expectation is that as the labor market continues to improve and households feel better about their financial condition that we will see household formation pick up and a somewhat stronger recovery than we've seen thus far in housing.

_____

The Special Note summarizes my overall thoughts about our economic situation

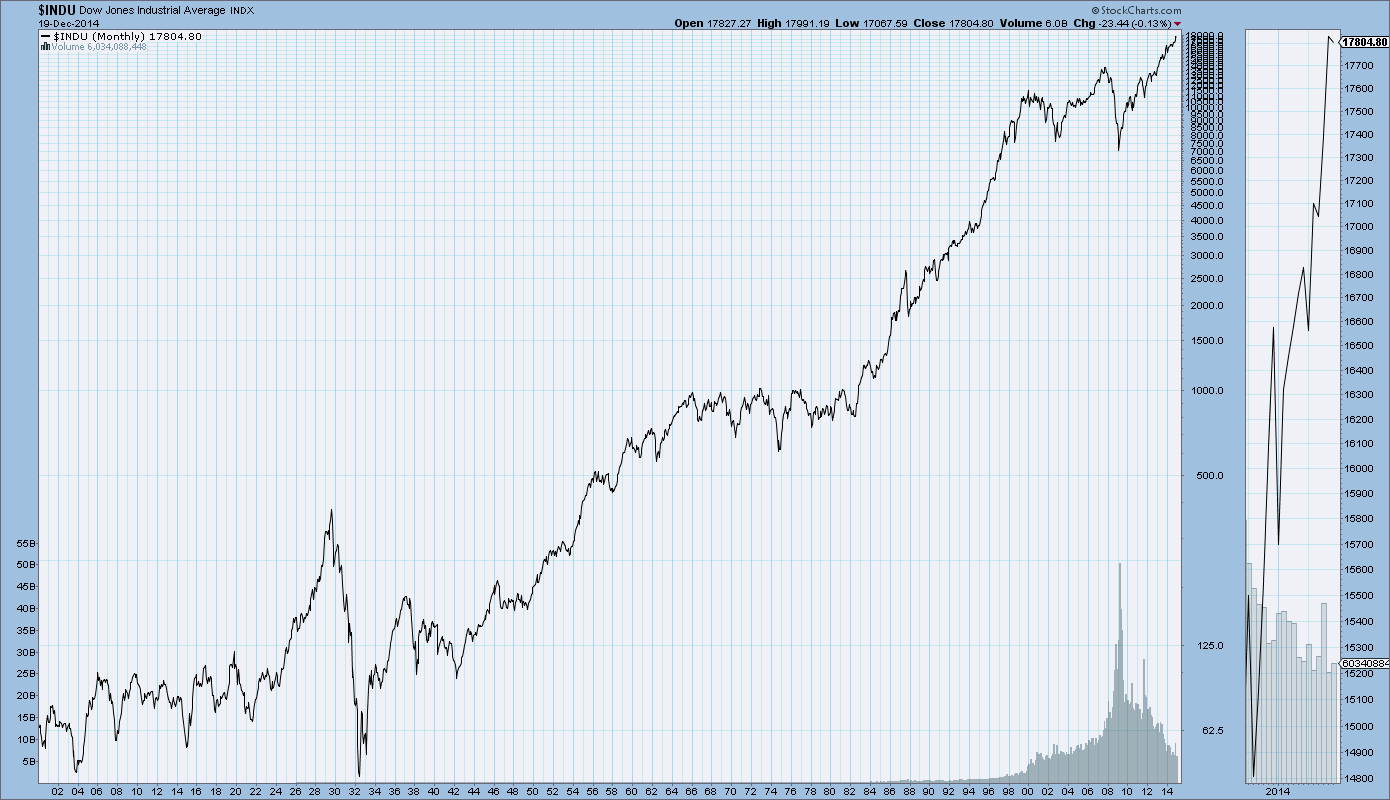

SPX at 2052.47 as this post is written