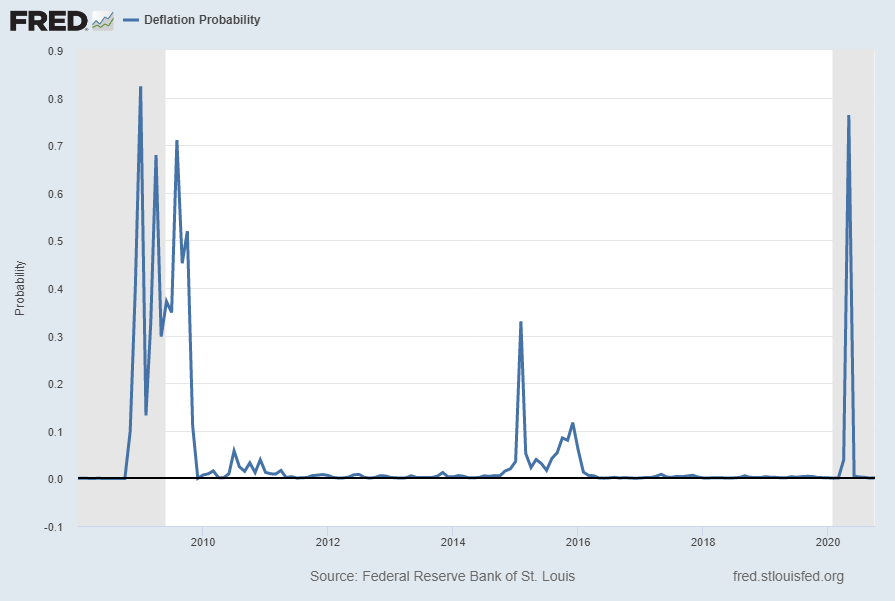

For reference, below is a chart of the St. Louis Fed Price Pressures Measures – Deflation Probability [FRED STLPPMDEF] through October 2020.

While I do not necessarily agree with the current readings of the measure, I view this as a proxy of U.S. deflation probability.

A description of this measure, as seen in FRED:

This series measures the probability that the personal consumption expenditures price index (PCEPI) inflation rate (12-month changes) over the next 12 months will fall below zero.

The chart, on a monthly basis from January 1990 – October 2020, with reading of .00127, last updated on October 30, 2020:

Here is this same deflation probability measure since 2008:

source: Federal Reserve Bank of St. Louis, Deflation Probability [STLPPMDEF], retrieved from FRED, Federal Reserve Bank of St. Louis; accessed October 30, 2020: https://fred.stlouisfed.org/series/STLPPMDEF

_________

I post various economic indicators and indices because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with what they depict or imply.

_____

The Special Note summarizes my overall thoughts about our economic situation

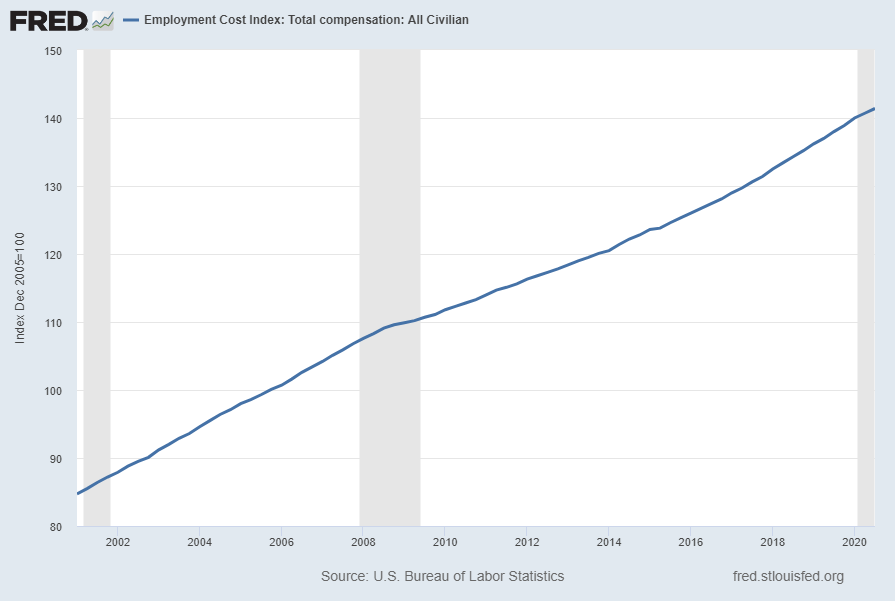

The Employment Cost Index (ECI) is a quarterly measure of the change in the price of labor, defined as compensation per employee hour worked. Closely watched by many economists, the ECI is an indicator of cost pressures within companies that could lead to price inflation for finished goods and services. The index measures changes in the cost of compensation not only for wages and salaries, but also for an extensive list of benefits. As a fixed-weight, or Laspeyres, index, the ECI controls for changes occurring over time in the industrial-occupational composition of employment.

On October 30, 2020, the ECI for the third quarter was released. Here are two excerpts from the BLS release titled “Employment Cost Index – September 2020“:

Compensation costs for civilian workers increased 0.5 percent, seasonally adjusted, for the 3-month period ending in September 2020, the U.S. Bureau of Labor Statistics reported today. Wages and salaries increased 0.4 percent and benefit costs increased 0.6 percent from June 2020. (See chart 1 and tables A, 1, 2, and 3.)

also:

Compensation costs for civilian workers increased 2.4 percent for the 12-month period ending in September 2020 and increased 2.8 percent in September 2019. Wages and salaries increased 2.5 percent over the year and increased 2.9 percent for the 12-month period ending in September 2019. Benefit costs increased 2.3 percent and also increased 2.3 percent for the 12-month period ending in September 2019. (See chart 2 and tables A, 4, 8, and 12.)

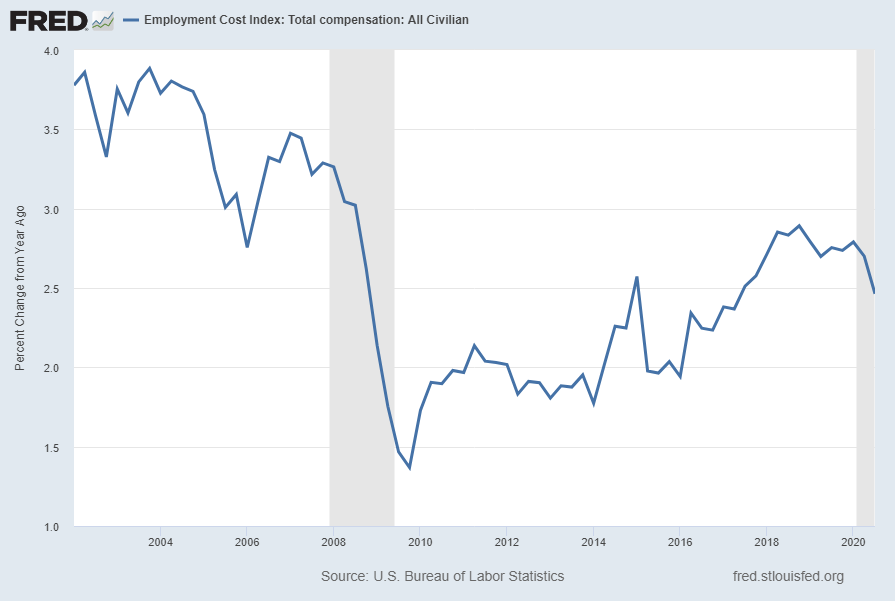

Below are three charts, updated on October 30, 2020 that depict various aspects of the ECI, which is seasonally adjusted (SA):

The first depicts the ECI, with a value of 141.4:

source: US. Bureau of Labor Statistics, Employment Cost Index: Total compensation: All Civilian [ECIALLCIV], retrieved from FRED, Federal Reserve Bank of St. Louis, accessed October 30, 2020: https://research.stlouisfed.org/fred2/series/ECIALLCIV/

The second chart depicts the ECI on a “Percent Change from Year Ago” basis, with a value of 2.5%:

The third chart depicts the ECI on a “Percent Change” (from last quarter) basis, with a value of .5%:

_________

I post various indicators and indices because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with what they depict or imply.

_____

The Special Note summarizes my overall thoughts about our economic situation

Each month I have been highlighting various estimates of U.S. recession probabilities. The latest update was that of October 7, 2020, titled “Recession Probability Models – October 2020.”

While I don’t agree with the methodologies employed or the probabilities of impending economic weakness as depicted by these and other estimates, I do believe that the results of these models and estimates should be monitored.

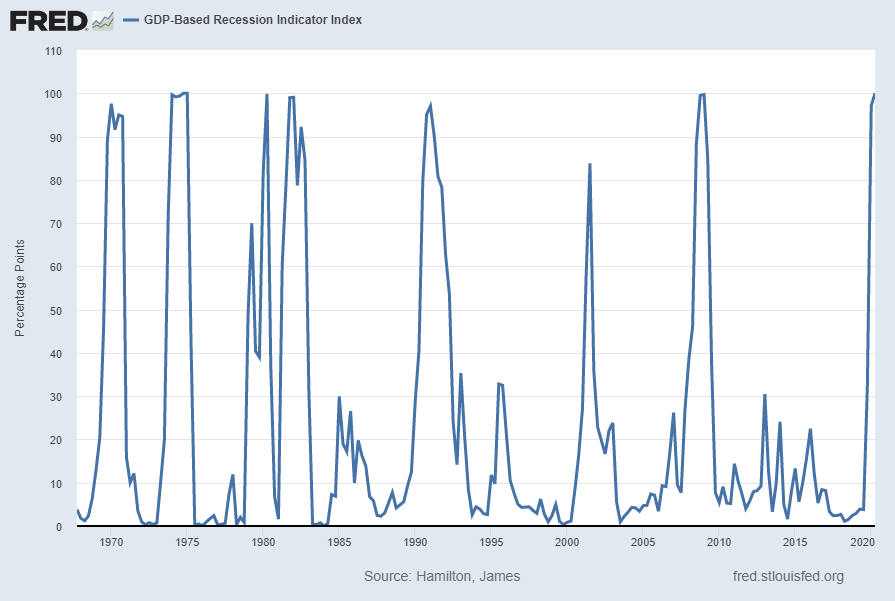

Another probability of recession is provided by James Hamilton, and it is titled “GDP-Based Recession Indicator Index.” A description of this index, as seen in FRED:

This index measures the probability that the U.S. economy was in a recession during the indicated quarter. It is based on a mathematical description of the way that recessions differ from expansions. The index corresponds to the probability (measured in percent) that the underlying true economic regime is one of recession based on the available data. Whereas the NBER business cycle dates are based on a subjective assessment of a variety of indicators that may not be released until several years after the event , this index is entirely mechanical, is based solely on currently available GDP data and is reported every quarter. Due to the possibility of data revisions and the challenges in accurately identifying the business cycle phase, the index is calculated for the quarter just preceding the most recently available GDP numbers. Once the index is calculated for that quarter, it is never subsequently revised. The value at every date was inferred using only data that were available one quarter after that date and as those data were reported at the time.

If the value of the index rises above 67% that is a historically reliable indicator that the economy has entered a recession. Once this threshold has been passed, if it falls below 33% that is a reliable indicator that the recession is over.

I post various indicators and indices because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with what they depict or imply.

_____

The Special Note summarizes my overall thoughts about our economic situation

I post various indicators and indices because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with what they depict or imply.

_____

The Special Note summarizes my overall thoughts about our economic situation

I post various indicators and indices because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with what they depict or imply.

_____

The Special Note summarizes my overall thoughts about our economic situation

The St. Louis Fed’s Financial Stress Index (STLFSI2) is one index that is supposed to measure stress in the financial system. Its reading as of the October 22, 2020 update (reflecting data through October 16, 2020) is -.3568.

Of course, there are a variety of other measures and indices that are supposed to measure financial stress and other related issues, both from the Federal Reserve as well as from private sources.

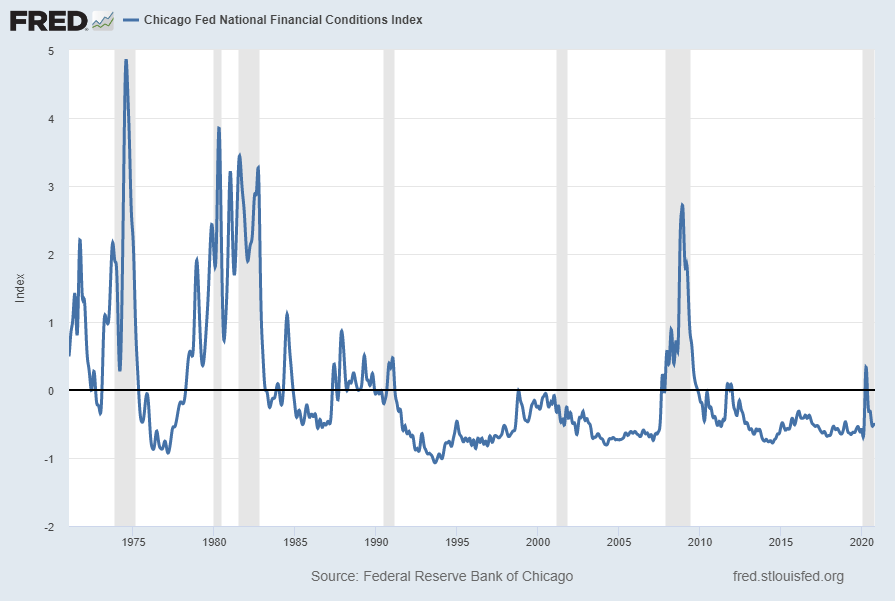

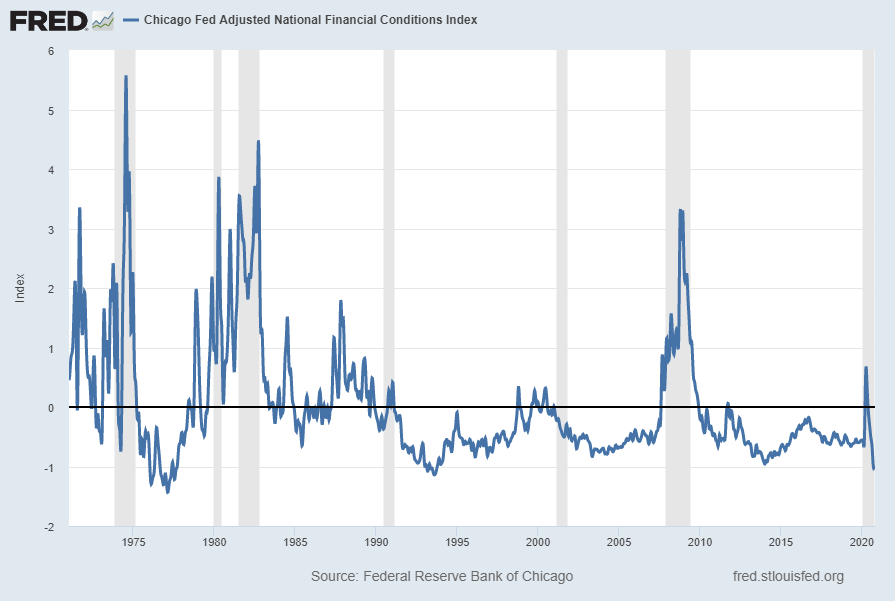

Two other indices that I regularly monitor include the Chicago Fed National Financial Conditions Index (NFCI) as well as the Chicago Fed Adjusted National Financial Conditions Index (ANFCI).

Here are summary descriptions of each, as seen in FRED:

The National Financial Conditions Index (NFCI) measures risk, liquidity and leverage in money markets and debt and equity markets as well as in the traditional and “shadow” banking systems. Positive values of the NFCI indicate financial conditions that are tighter than average, while negative values indicate financial conditions that are looser than average.

The adjusted NFCI (ANFCI). This index isolates a component of financial conditions uncorrelated with economic conditions to provide an update on how financial conditions compare with current economic conditions.

For further information, please visit the Federal Reserve Bank of Chicago’s web site:

Below are the most recently updated charts of the NFCI and ANFCI, respectively.

The NFCI chart below was last updated on October 28, 2020 incorporating data from January 8, 1971 through October 23, 2020, on a weekly basis. The October 23 value is -.51891:

The ANFCI chart below was last updated on October 28, 2020 incorporating data from January 8, 1971 through October 23, 2020, on a weekly basis. The October 23, 2020 value is -1.01379:

I post various indicators and indices because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with what they depict or imply.

_____

The Special Note summarizes my overall thoughts about our economic situation

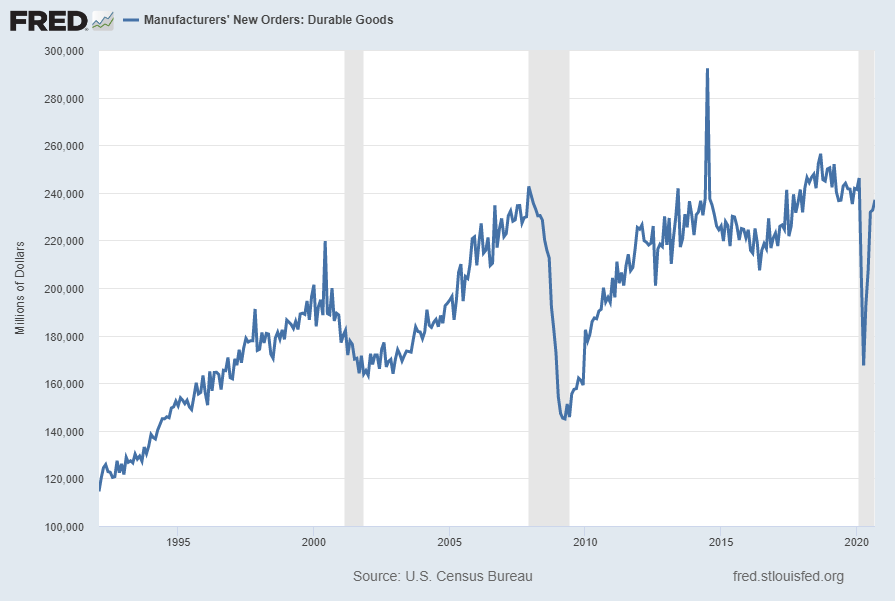

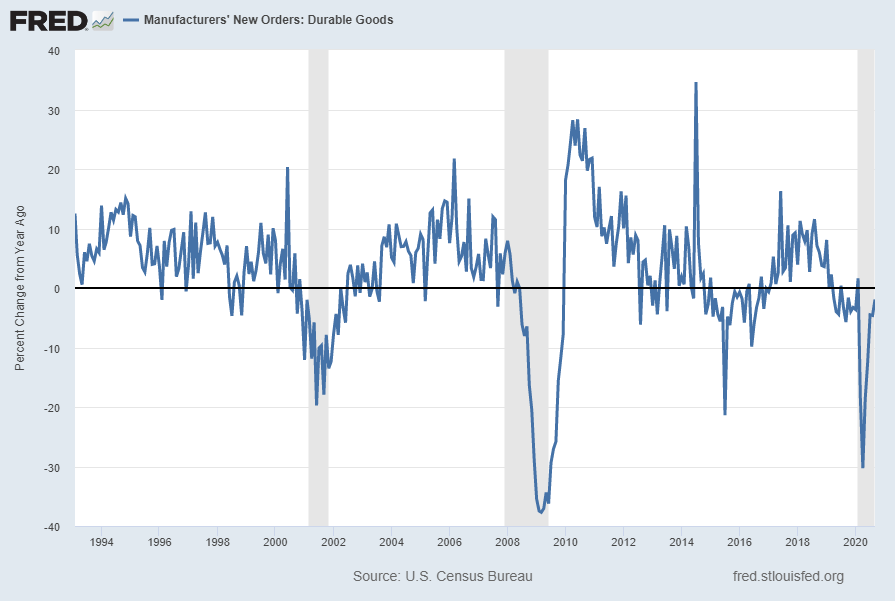

Many people place emphasis on Durable Goods New Orders as a prominent economic indicator and/or leading economic indicator.

For reference, below are two charts depicting this measure.

First, from the St. Louis Fed site (FRED), a chart through September 2020, updated on October 27, 2020. This value is $237,057 ($ Millions):

(click on charts to enlarge images)

–

Second, here is the chart depicting this measure on a “Percentage Change from a Year Ago” basis, with a last value of -1.9%:

Data Source: FRED, Federal Reserve Economic Data, Federal Reserve Bank of St. Louis: Manufacturers’ New Orders: Durable Goods [DGORDER]; U.S. Department of Commerce: Census Bureau; accessed October 27, 2020; http://research.stlouisfed.org/fred2/series/DGORDER

_________

I post various indicators and indices because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with what they depict or imply.

_____

The Special Note summarizes my overall thoughts about our economic situation

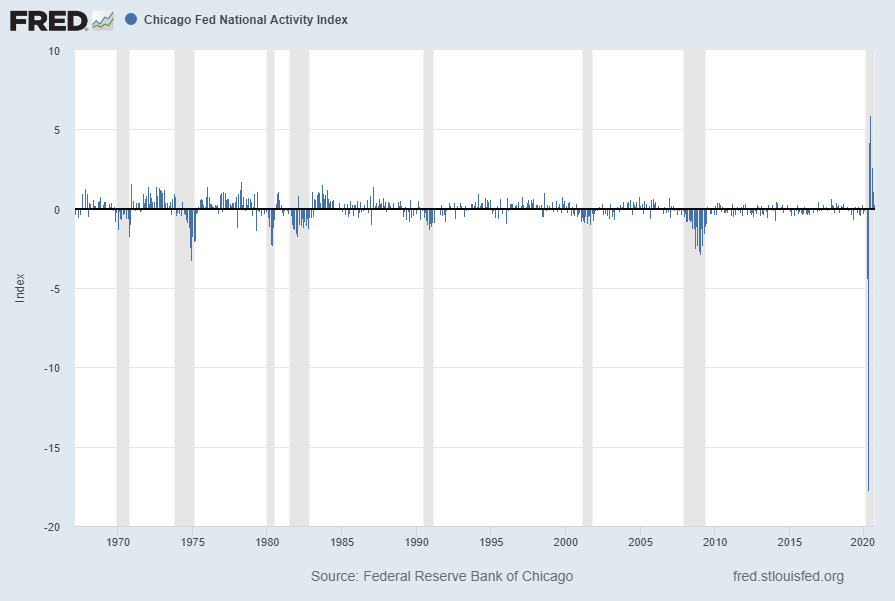

The following is an update of various indicators that are supposed to predict and/or depict economic activity. These indicators have been discussed in previous blog posts:

source: Federal Reserve Bank of Chicago, Chicago Fed National Activity Index [CFNAI], retrieved from FRED, Federal Reserve Bank of St. Louis, October 26, 2020; https://fred.stlouisfed.org/series/CFNAI

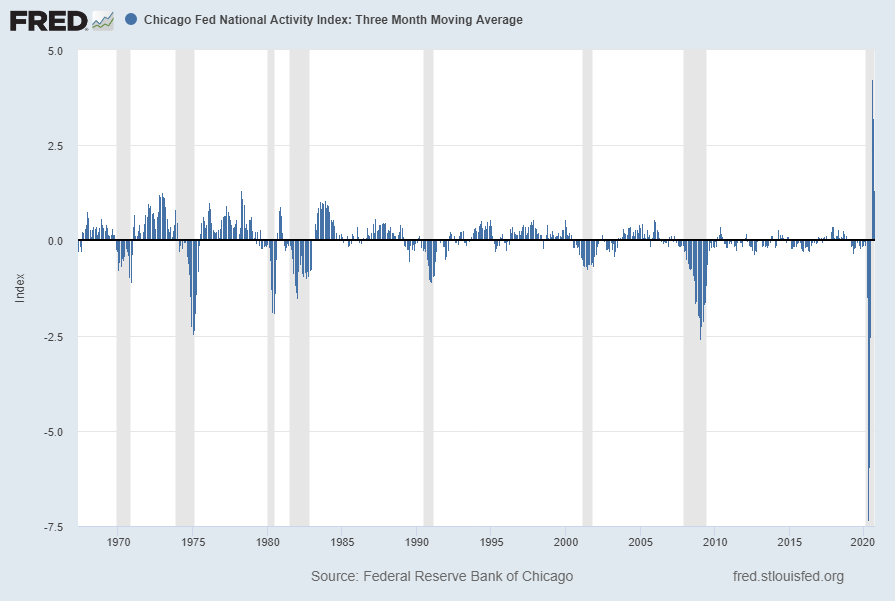

The CFNAI-MA3, with a current reading of 1.33:

source: Federal Reserve Bank of Chicago, Chicago Fed National Activity Index: Three Month Moving Average [CFNAIMA3], retrieved from FRED, Federal Reserve Bank of St. Louis, October 26, 2020; https://fred.stlouisfed.org/series/CFNAIMA3

The Conference Board Leading (LEI), Coincident (CEI) Economic Indexes, and Lagging Economic Indicator (LAG):

As per the October 22, 2020 Conference Board press release, titled “The Conference Board Leading Economic Index (LEI) for the U.S. Increased in September” the LEI was at 107.2, the CEI was at 101.7, and the LAG was 107.6 in September.

An excerpt from the release:

“The US LEI increased in September, driven primarily by declining unemployment claims and rising housing permits. However, the decelerating pace of improvement suggests the US economy could be losing momentum heading into the final quarter of 2020,” said Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board. “The US economy is projected to expand in Q4, but at a substantially slower rate of 1.5 percent (annual rate) according to The Conference Board’s GDP forecast. Furthermore, downside risks to the recovery may be increasing amid rising new cases of COVID-19 and continued labor market weakness.”

_________

I post various indicators and indices because I believe they should be carefully monitored. However, as those familiar with this site are aware, I do not necessarily agree with what they depict or imply.

_____

The Special Note summarizes my overall thoughts about our economic situation

Perhaps the main reason that I write of our economic situation is that I continue to believe, based upon various analyses, that our economic situation is in many ways misunderstood. While no one likes to contemplate a future rife with economic adversity, current and future economic problems must be properly recognized and rectified if high-quality, sustainable long-term economic vitality is to be realized.

There are an array of indications and other “warning signs” – many readily apparent – that current economic activity and financial market performance is accompanied by exceedingly perilous dynamics.

I have written extensively about this peril, including in the following:

My analyses continues to indicate that the growing level of financial danger will lead to the next stock market crash that will also involve (as seen in 2008) various other markets as well. Key attributes of this next crash is its outsized magnitude (when viewed from an ultra-long term historical perspective) and the resulting economic impact. This next financial crash is of tremendous concern, as my analyses indicate it will lead to a Super Depression – i.e. an economy characterized by deeply embedded, highly complex, and difficult-to-solve problems.

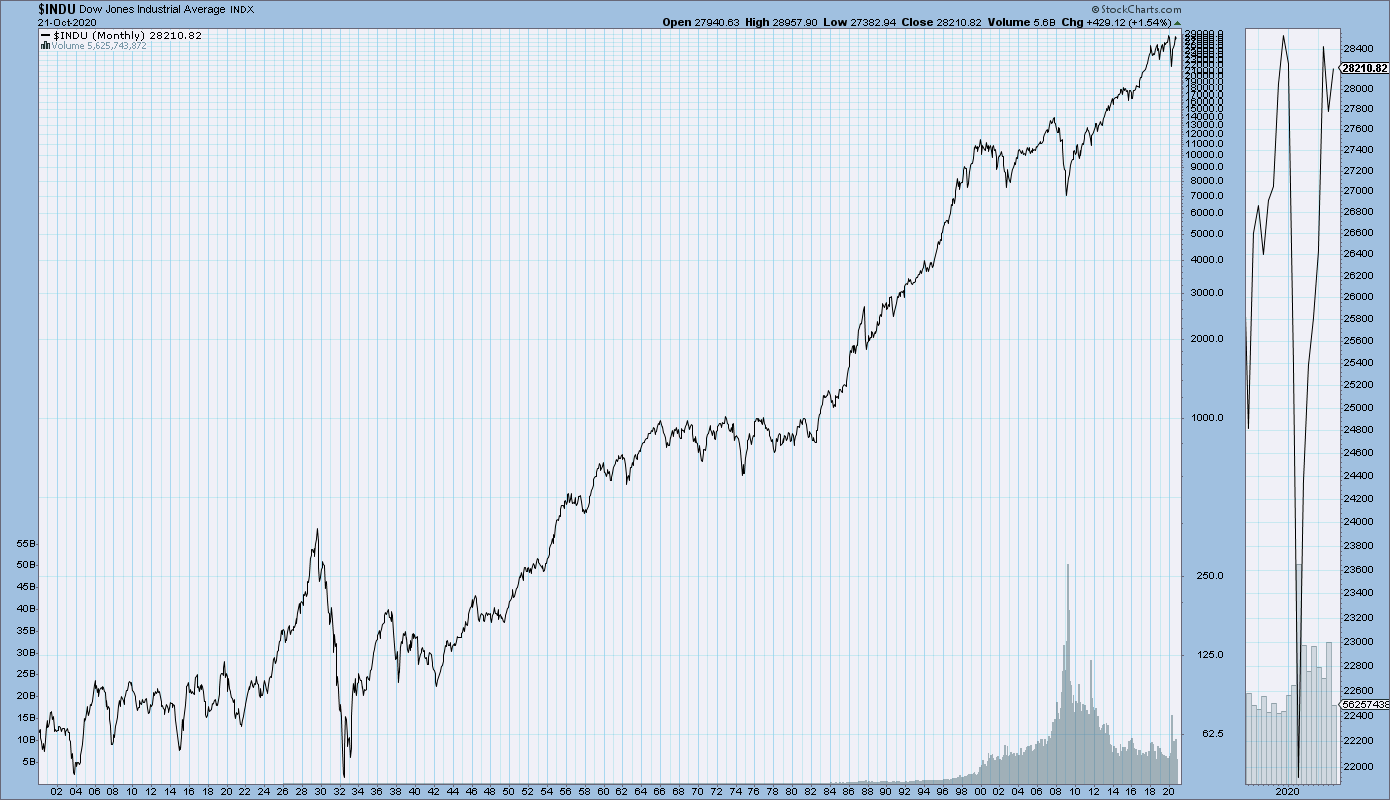

For long-term reference purposes, here is a chart of the Dow Jones Industrial Average since 1900, depicted on a monthly basis using a LOG scale (updated through October 21, 2020, with a last value of 28210.82):

(click on chart to enlarge image)(chart courtesy of StockCharts.com)

_____

The Special Note summarizes my overall thoughts about our economic situation

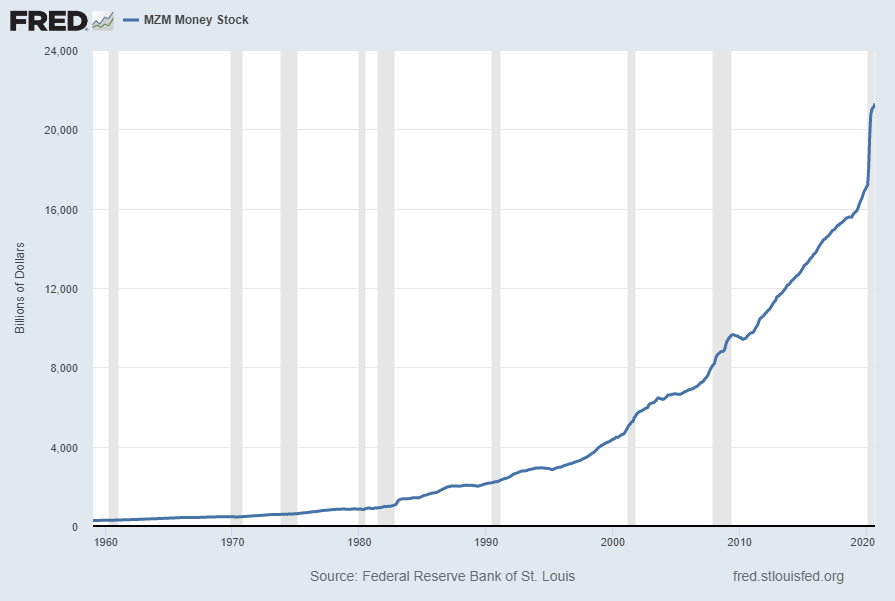

For reference purposes, below are two sets of charts depicting growth in the money supply.

The first shows the MZM (Money Zero Maturity), defined in FRED as the following:

M2 less small-denomination time deposits plus institutional money funds. Money Zero Maturity is calculated by the Federal Reserve Bank of St. Louis.

Here is the “MZM Money Stock” (seasonally adjusted) chart, updated on October 15, 2020 depicting data through September 2020, with a value of $21,301.9 Billion:

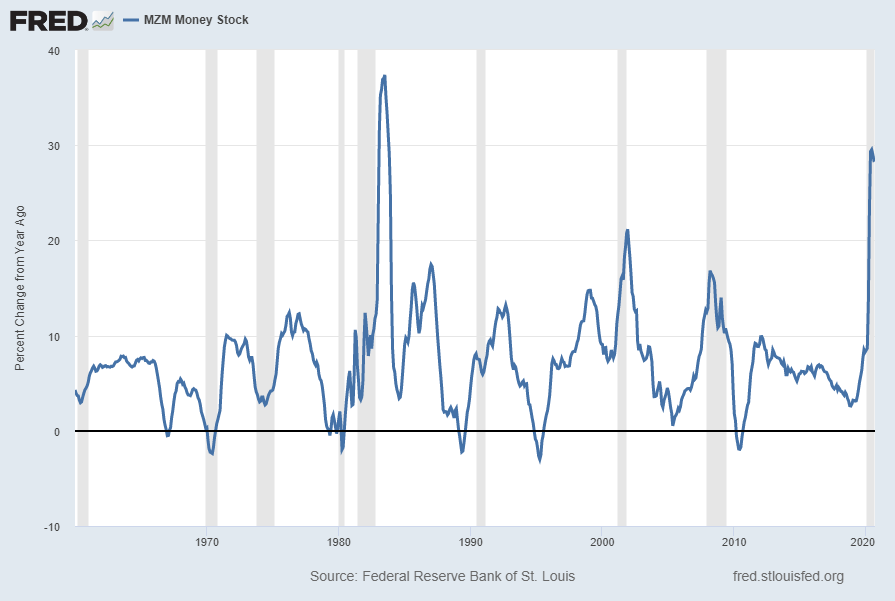

Here is the “MZM Money Stock” chart on a “Percent Change From Year Ago” basis, with a current value of 28.5%:

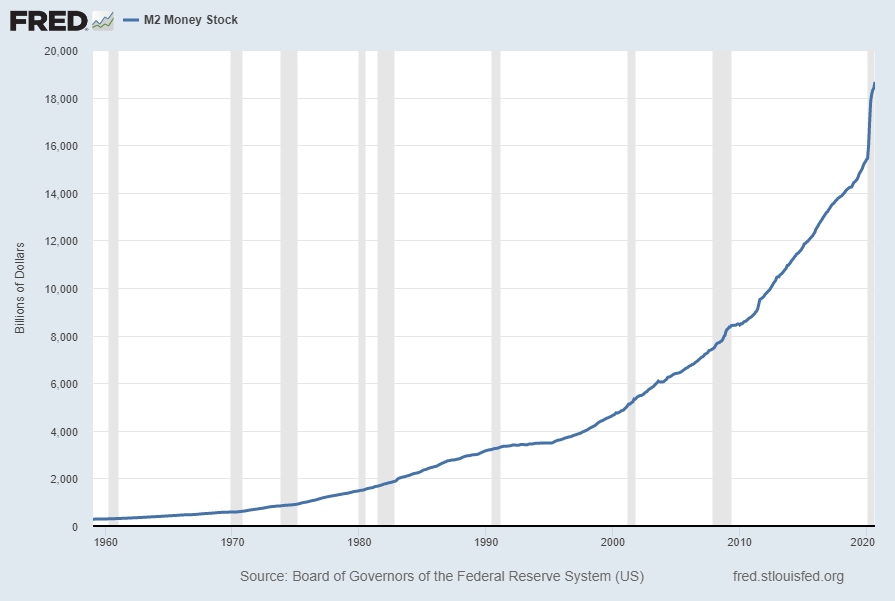

The second set shows M2, defined in FRED as the following:

M2 includes a broader set of financial assets held principally by households. M2 consists of M1 plus: (1) savings deposits (which include money market deposit accounts, or MMDAs); (2) small-denomination time deposits (time deposits in amounts of less than $100,000); and (3) balances in retail money market mutual funds (MMMFs). Seasonally adjusted M2 is computed by summing savings deposits, small-denomination time deposits, and retail MMMFs, each seasonally adjusted separately, and adding this result to seasonally adjusted M1.

Here is the “M2 Money Stock” (seasonally adjusted) chart, updated on October 15, 2020, depicting data through September 2020, with a value of $18,658.1 Billion:

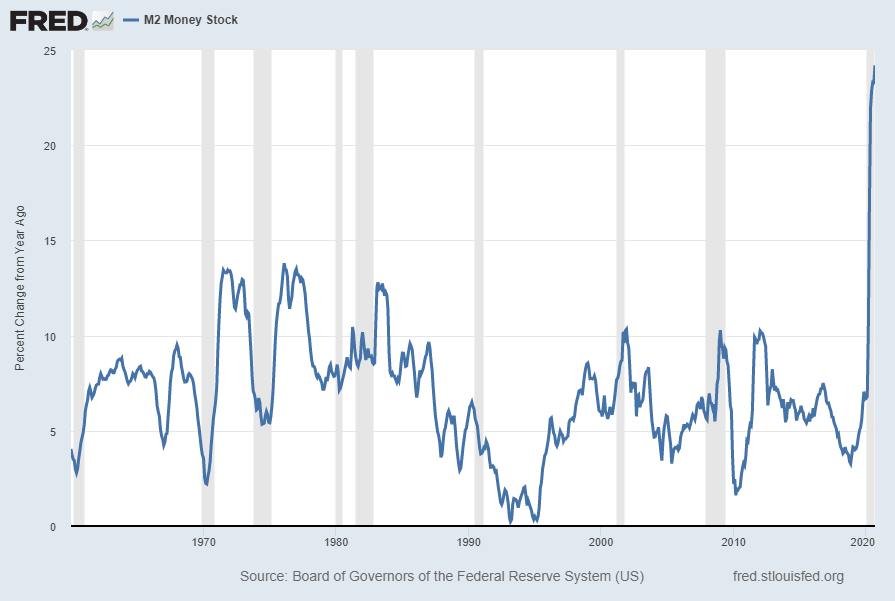

Here is the “M2 Money Stock” chart on a “Percent Change From Year Ago” basis, with a current value of 24.2%: