Throughout this site there are many discussions of economic indicators. This post is the latest in a series of posts indicating facets of U.S. economic weakness or a notably low growth rate.

The level and trend of economic growth is especially notable at this time. As seen in various measures and near-term projections, the U.S. economy had undergone an outsized level of economic contraction in 2020. However, most people believe (and virtually all prominent economic forecasts indicate) that this historic level of contraction will have proven ephemeral in nature; i.e. an economic expansion will continue.

As seen in the January 2022 Wall Street Journal Economic Forecast Survey the consensus (average estimate) among various economists is for 3.30% GDP growth in 2022, 2.42% GDP growth in 2023, and 2.22% GDP growth in 2024.

Charts Indicating U.S. Economic Weakness

Below are a small sampling of charts that depict weak growth or contraction, and a brief comment for each:

__

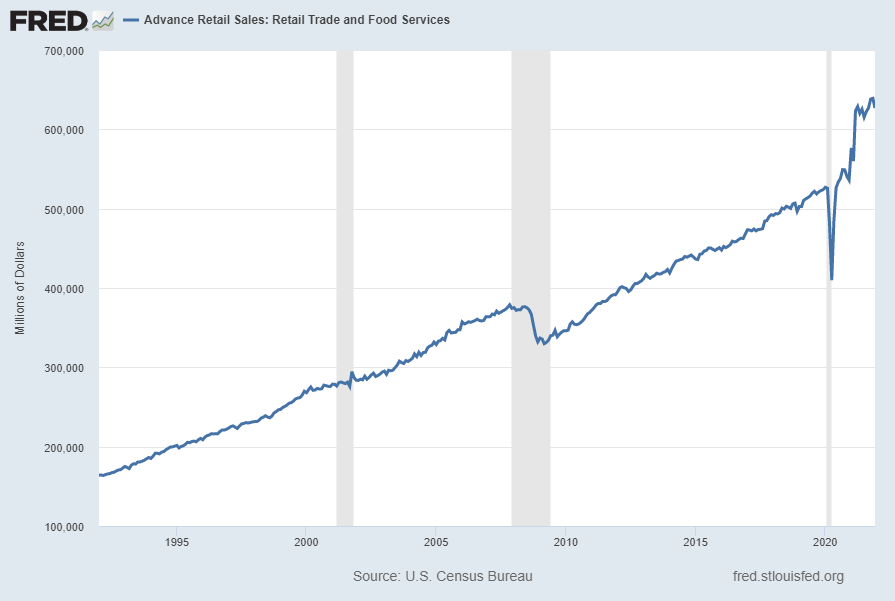

Advance Retail Sales: Retail Trade and Food Services (RSAFS)

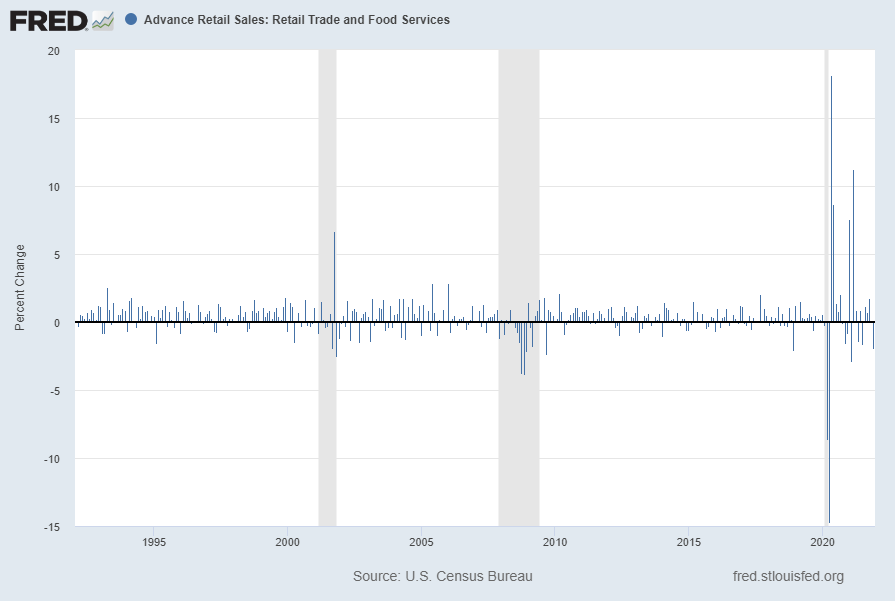

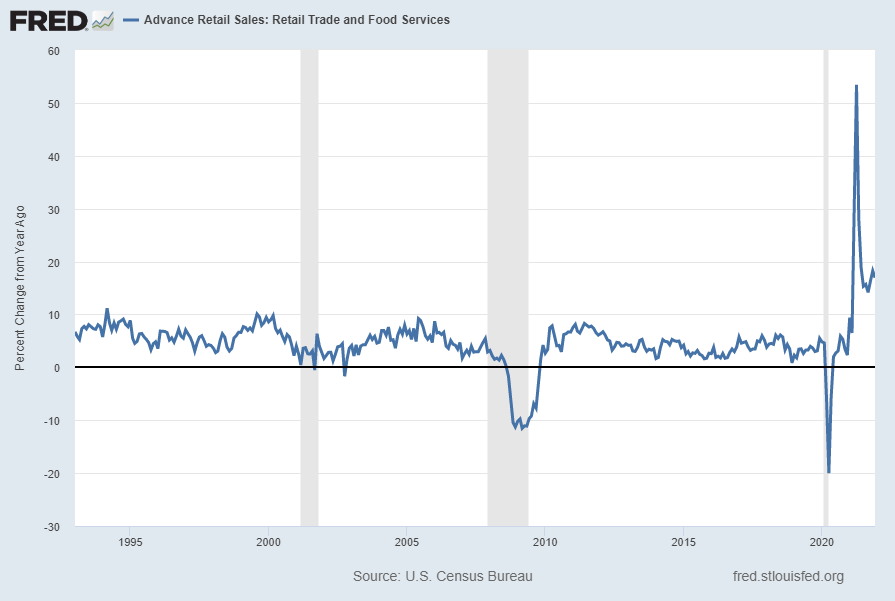

Advance Retail Sales: Retail Trade and Food Services (RSAFS), when viewed from a long-term perspective, has recently been volatile. While the trend when viewed from a “Percent Change From Year Ago” basis remains – as one might expect – robust, when viewed from a “Percent Change” (from the prior month) basis the growth trend appears less robust.

Shown below is this measure with last value of $626,833 Million through December, last updated January 14, 2022:

Displayed below is this same RSAFS measure on a “Percent Change” (from prior month) basis with value -1.9%:

Below is this measure displayed on a “Percent Change From Year Ago” basis with value 16.9%:

source: U.S. Census Bureau, Advance Retail Sales: Retail and Food Services, Total [RSAFS], retrieved from FRED, Federal Reserve Bank of St. Louis; accessed February 9, 2022: https://fred.stlouisfed.org/series/RSAFS

__

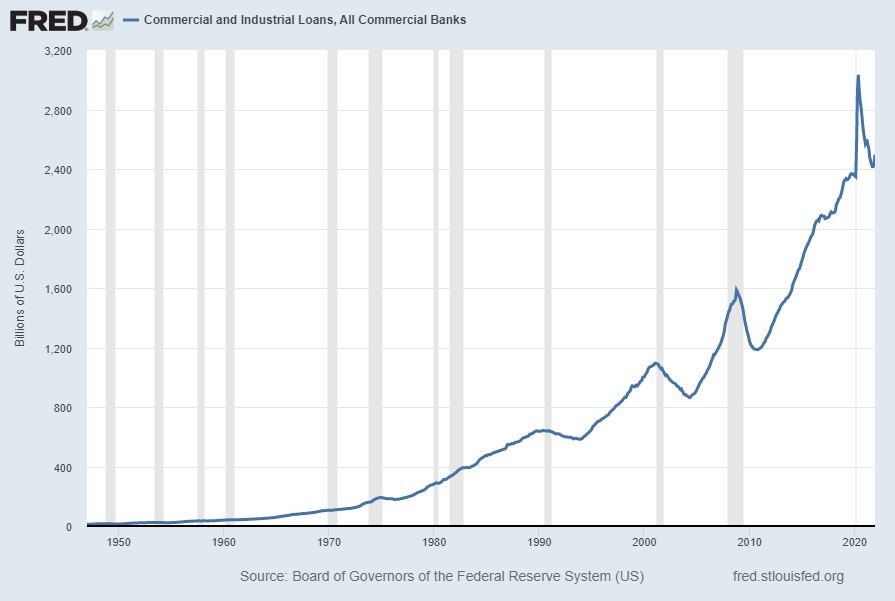

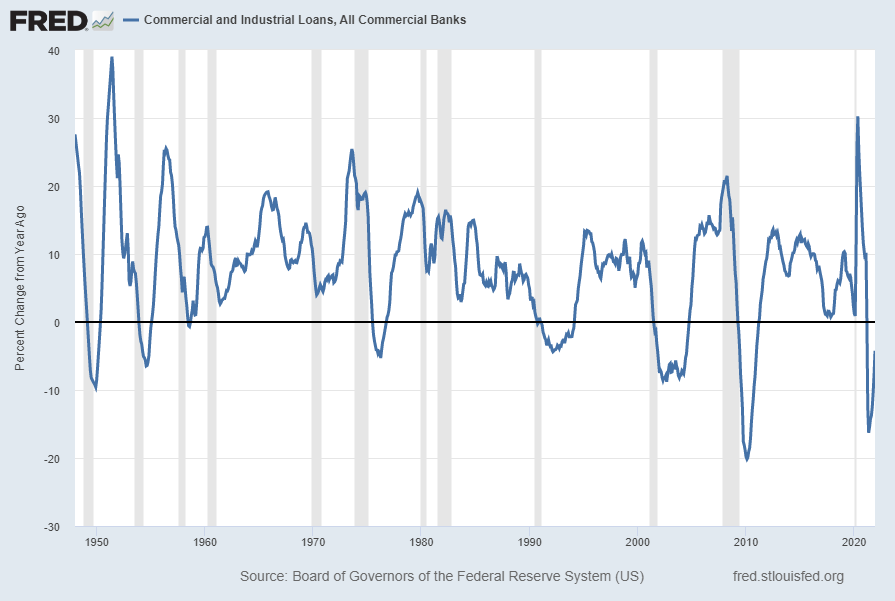

Commercial And Industrial Loans, All Commercial Banks (BUSLOANS)

“Commercial And Industrial Loans, All Commercial Banks” (BUSLOANS) has recently been volatile. Shown below is this measure with last value of $2,495.7226 Billion through December 2021, last updated February 4, 2022:

Below is this measure displayed on a “Percent Change From Year Ago” basis with value -4.2%:

source: Board of Governors of the Federal Reserve System (US), Commercial and Industrial Loans, All Commercial Banks [BUSLOANS], retrieved from FRED, Federal Reserve Bank of St. Louis; accessed February 9, 2022: https://fred.stlouisfed.org/series/BUSLOANS

__

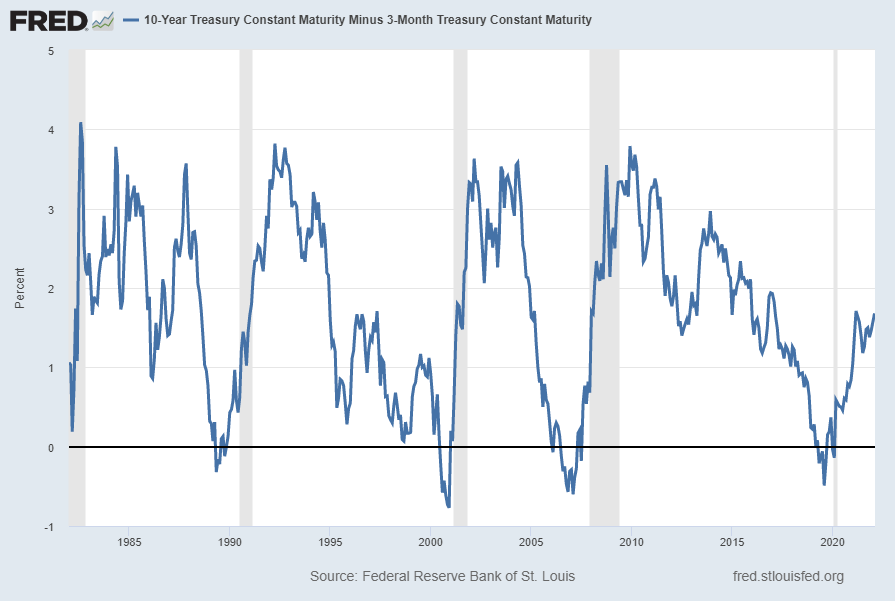

The Yield Curve

Many people believe that the Yield Curve is a leading economic indicator for the United States economy.

On March 1, 2010, I wrote a post on the issue, titled “The Yield Curve As A Leading Economic Indicator.”

While I continue to have the stated reservations regarding the “Yield Curve” as an indicator, I do believe that it should be monitored.

The U.S. Yield Curve (one proxy seen below) while positive, is (all things considered) relatively low when viewed from a long-term perspective. Below is the spread between the 10-Year Treasury Constant Maturity and the 3-Month Treasury Constant Maturity from 1982 through the February 9, 2022 value, showing a value of 1.68% [10-Year Treasury Yield (FRED DGS10) of 1.96% as of February 8, 3-Month Treasury Yield (FRED DGS3MO) of .25% as of February 8]:

source: Federal Reserve Bank of St. Louis, 10-Year Treasury Constant Maturity Minus 3-Month Treasury Constant Maturity [T10Y3M], retrieved from FRED, Federal Reserve Bank of St. Louis; accessed February 9, 2022: https://fred.stlouisfed.org/series/T10Y3M

__

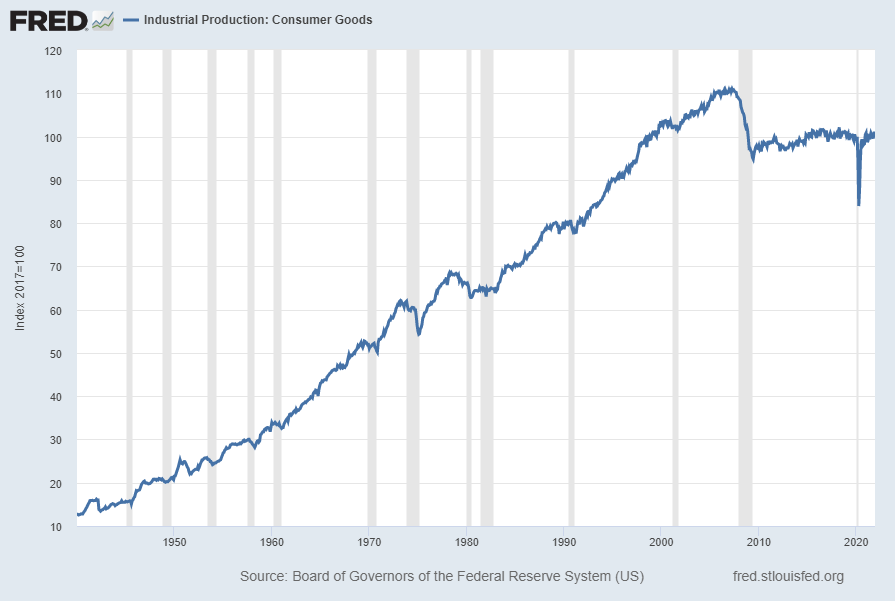

Industrial Production: Consumer Goods (IPCONGD)

The “Industrial Production: Consumer Goods” measure has been relatively subdued since the Financial Crisis. Shown below is a long-term chart of this measure (displayed from 1939), with last value of 100.1636 through December 2021, last updated January 14, 2022:

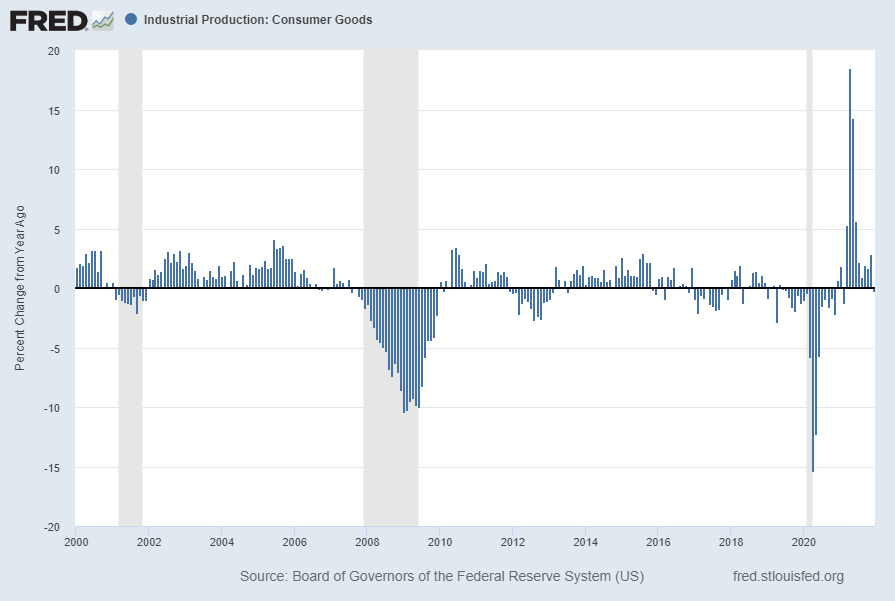

Displayed below is this same IPCONGD measure on a “Percent Change From Year Ago” basis. The current value is -.2%:

source: Board of Governors of the Federal Reserve System (US), Industrial Production: Consumer Goods [IPCONGD], retrieved from FRED, Federal Reserve Bank of St. Louis; accessed February 9, 2022: https://fred.stlouisfed.org/series/IPCONGD

__

Other Indicators

As mentioned previously, many other indicators discussed on this site indicate slow economic growth or economic contraction, if not outright (gravely) problematical economic conditions.

_____

The Special Note summarizes my overall thoughts about our economic situation

SPX at 4587.18 as this post is written

No comments:

Post a Comment